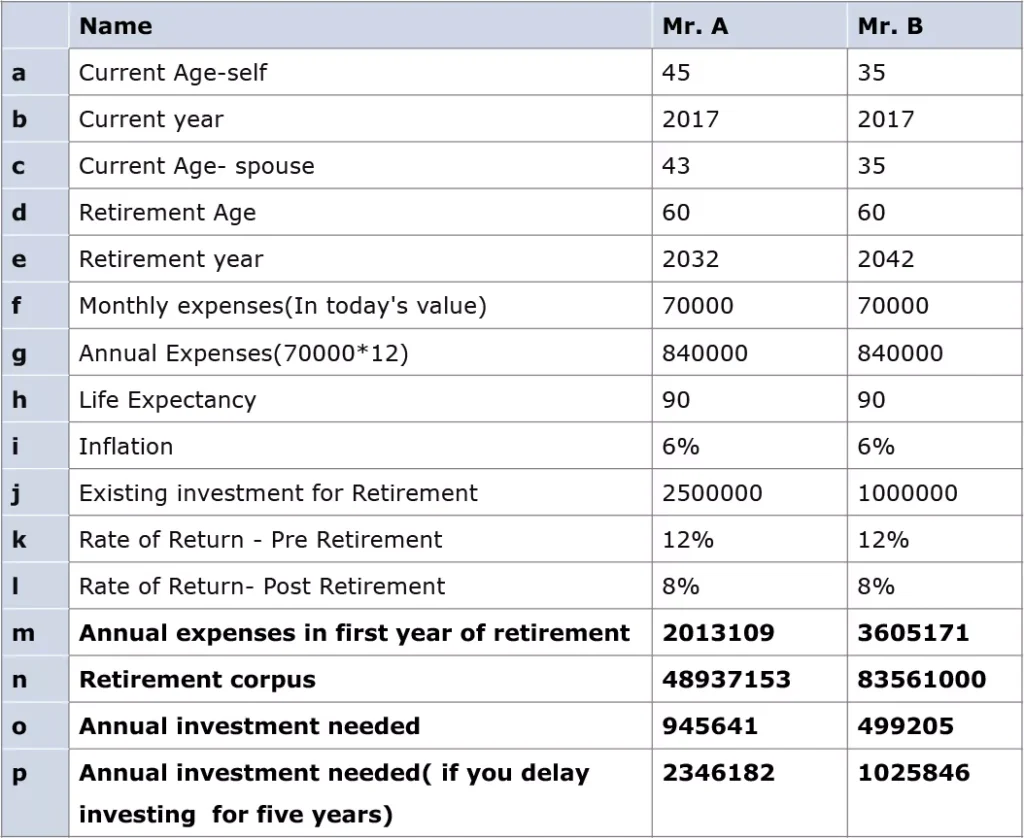

In my last article I discussed about the importance of Retirement Planning, in this issue I would like to discuss on how to plan your retirement. So here I would like to help readers with some numbers. For that here below I am discussing two illustrations for Retirement planning, first one with an age of 45 years of Mr. A and second with an age of 35 years of Mr. B. In first case, age of spouse is purposefully taken at 43 and in second case age of spouse is taken same 35 years.

Kindly remember that every individual’s numbers may change and this example is just a basic illustrative example and I have not taken any complications in this so don’t adopt these figures for your retirement planning directly.

In above illustration I have calculated retirement corpus for Mr. A, who is 45 years old and his wife is 43 years old. Retirement age is taken as 60 so retirement year is 2032 & years to retirement are only 15. Now as you can see that with life expectancy of 90 years and spouse’s age being 43 the total retirement years to support from retirement corpus would be 32.

- In the second case of Mr. B, his age is 35 and spouse’s age is also taken as 35 and retirement age is same 60 so years to retirement would be 25 but total retirement years to support would be 30 only.

- In above table, blocks with light blue background are the blocks which are input blocks. These are to be decided & filled up and the blocks shown with dark blue background are output blocks which come as a result of calculations.

- Monthly Expenses: In the monthly expense block (f) one has to fill the monthly expenses at current rate if you are retired today. These are the expenses of monthly nature like light bills, telephone bills, petrol bills, grocery expense etc. everything that is of monthly nature. One can also add other annual expenses like travelling etc. by dividing it to 12. Kindly remember that this is the figure that if you retire today then this will be your monthly expenses in today’s value. So while calculating this one has to consider that children are settled at the time retirement so deduct all expenses related to children from your current monthly expenses. Add few expenses like medical cost and additional cost for servants needed in the old age. In both above cases, I have taken this as Rs. 70000 monthly and in block (g) above I have converted them to annual to make calculations easy. So annual expenses required in today’s value to retire are Rs. 840000. Further at 6%(h) inflation you can see that for Mr. A it becomes Rs.2013109 where as for Mr. B it becomes Rs. 3605171 this happens because in case of Mr. B he is 35 year old and years to retirement are 25 as compared to Mr. A where years to retirement are 15 so for Mr. B inflation has more impact. So if you’re annual expenses is Rs. 840000 today it will be 20 lakhs after 15 years and 36 lakhs after 25 years. This will be just first year retirement expense and it will keep increasing every year with increasing inflation.

- Retirement Corpus: To live a comfortable retired life the total Corpus needed at the time of Retirement (2032) for Mr. A is Rs. 4.89 crores (approx.) and for Mr. B in 2042 would be Rs. 8.35 crores (approx) shown in cell N in above table.

- Rate of Return on Investments: Also it is assumed that both Mr. A & Mr. B will earn 12% (cell k)post tax returns on their total portfolio pre retirement and 8% (cell I) post tax returns on their portfolio post retirement.

- Existing investment & Annual investment needed : It is assumed that Mr. A has already provided Rs. 25 lakhs (cell j)for his retirement and Mr. B has already provided Rs. 10 lakhs. So considering that Mr. A is required to make annual investment of Rs.9.45 lakhs (ap.) (from 45 age to 60 age) (cell) to achieve the needed retirement corpus and Mr. B is required to make annual investment of Rs. 4.99 lakhs (app.) (from 35 age to 60 age) to achieve needed retirement corpus. So even though Mr. B’s needed retirement corpus is almost double than that of Mr. A his annual investment required is almost half. This is because he has 25 years left to his retirement from now where as Mr. A has only 15 years left out to his retirement.

- Delay in Retirement Planning : last figure in cell p shows that if Mr. A & Mr. B both decide to delay their retirement planning decision by further 5 years and want to start providing for retirement after 5 year then what would be the annual investment required to meet the same target retirement corpus at 60. In case of Mr. A the annual investment needed if he starts after 5 years is 23.46 Lakhs which is more than double as compared to figure of 9.45 lakhs if he starts now. And for Mr. B it is Rs. 10.25 Lakhs against Rs. 4.99 lakhs if he starts now. So five years delay can make this goal very difficult.

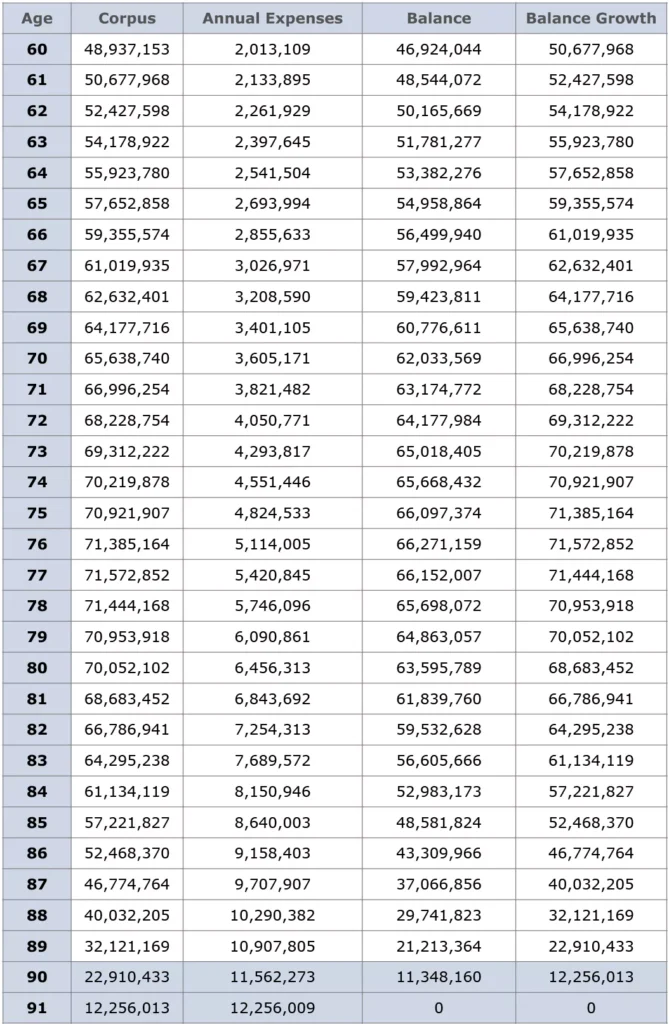

Below is the corpus utilization table for above illustration of Mr. A which shows how annual expenses keep growing even after retirement and how corpus is utilized for the same. At 92 years of age of wife the corpus becomes zero.

This happens because till 76 years of age annual expenses are less than return earned from the retirement portfolio and so retirement portfolio is increasing till that time but after 76 years of age you can see that retirement corpus starts reducing every year because annual expenses are more than return from retirement portfolio.

Retirement Corpus Utilization Table

Conclusion: Following are few points which one should keep in mind from above discussion.

1) Retirement is last but important Goal: generally retirement is last goal by time in the life of most of people but it is most important goal as we have to support long retirement years without regular income from primary source.

2) Start Early: Figures of retirement corpus & annual investment needed looks very big but if you start early it is not that difficult and you can achieve it easily. But if you delay your decision for planning and providing for retirement it can become dangerous.

3) Be Consistent : Most of the people when they start providing for retirement they don’t remain consistent in their strategy or sometimes don’t invest consistently and stop in between. This can disturb your retirement planning so keep investing consistently.

4) Calculate for yourself: If any of you want to make such calculation for yourself then kindly mail me on lohana_prakash@ascentsolutions.in . I need your current age, Spouse’s current age, retirement age, Monthly expenses in today’s value, existing provision for retirement if any. Rest of the things we will assume and give you figures of Needed Retirement Corpus & Annual investment. On receipt of above data my team will revert in two working days.