Warren Buffett, widely regarded as one of the most successful investors of all time, famously said, “Rule No. 1: Never lose money. Rule No. 2: Never forget rule No. 1.” This simple yet powerful quote encapsulates one of Buffett’s key principles when it comes to investing and wealth preservation.

Even though equity is one of the best performing asset classes, the penetration has been low in India. Furthermore, whenever the penetration has increased significantly, it is mostly during high valuation periods.

The primary cause of such low penetration may be volatility and concerns over the safety of capital, which makes safety of capital an important parameter. Just like in ancient times, gladiators used to carry a shield along with a sword for protection. Similarly, in the modern world, the strongest army requires a great defense system to ensure their safety and security.

Why is ensuring safety the first step towards wealth creation?

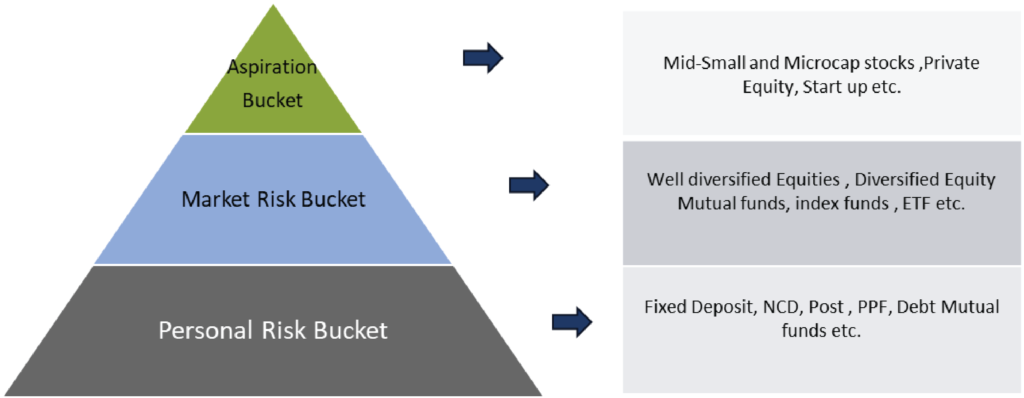

If we consider a typical investor portfolio, there are three risk buckets that an investor consciously or subconsciously manages:

– Personal risk bucket

– Market risk bucket

– Aspirational risk bucket

Personal Risk Bucket is the allocation which ensures that investors do not have to compromise their current lifestyle. Hence, it forms a major part of the investor’s portfolio. Traditionally, investors used to keep this money in post office savings, Public Provident Fund (PPF), bonds, fixed deposits (FDs), and debt mutual funds.

Next is the Market Risk Bucket, where investors allocate a lesser amount compared to the previous bucket. This allocation allows the investor to maintain or slightly improve their lifestyle if it outperforms significantly. Large-cap equities, diversified equity mutual funds, and index funds generally fall into this bucket. The overall allocation in this bucket is lower, so it cannot create a significant change in the overall portfolio returns.

The third bucket, which receives a minuscule capital investment, is referred to as the Aspirational bucket. It is not exactly like playing the lottery, but a positive outcome can bring a dramatic improvement in someone’s wealth. It can move an individual’s lifestyle up by two to three levels on the ladder. However, if things go wrong, the impact can be insignificant as it is a very small part of the portfolio. It can be considered a low probability and high impact investment outcome. Investments in micro-cap stocks, private equity, venture capital, or startups typically fall into this category.

How to Optimize the Portfolio return

Now, without enhancing the performance of the personal risk bucket, it is nearly impossible to increase the performance of an investor’s overall portfolio, as it is one of the biggest and core parts of the investor’s portfolio. Equity is one of the asset classes that can be considered for this purpose. However, the challenge with equity is that it also adds significant risk to the overall portfolio.

Investing can be likened to driving a car, where acceleration is similar to investing in equities. However, one cannot keep accelerating continuously as there are dangerous curves and traffic on the road. That’s why cars have brakes to calibrate speed as needed. In this analogy, brakes can be compared to fixed income investments. Nonetheless, there is still a risk that someone else may collide with your car. To handle such situations, we need to have airbags in the car. At the portfolio level, allocation to gold is required to withstand such crises. In this context, equity acts as acceleration, fixed income acts as brakes, and gold acts as an airbag.

During volatile periods, fixed income investments act as volatility controllers, while during crises like the subprime and Covid, gold acts as a volatility absorber. Its prices appreciate dramatically during such times, thereby helping the portfolio absorb the shocks.

Combining Asset classes through Multi Asset Strategy to optimize return at given level of volatility.

Various asset classes have a varied degree of correlation with each other. Economic cycles and markets across the globe are highly dynamic, making it difficult to consistently time the winning asset class. However, a well-balanced mix of these asset classes can assist investors in achieving an optimum level of risk-adjusted return to reach their long-term financial goals.

Just for example, based on the data taken from Jan 2010 to Apr 2023, there is a correlation of -0.22 between Equity and Debt, -0.55 between Equity and Gold, and -0.05 between Debt and Gold. By combining these asset classes in a scientific manner, it is possible to achieve a desired level of volatility. In fact, the volatility of the portfolio would be lower than the aggregate volatility of the individual asset classes.

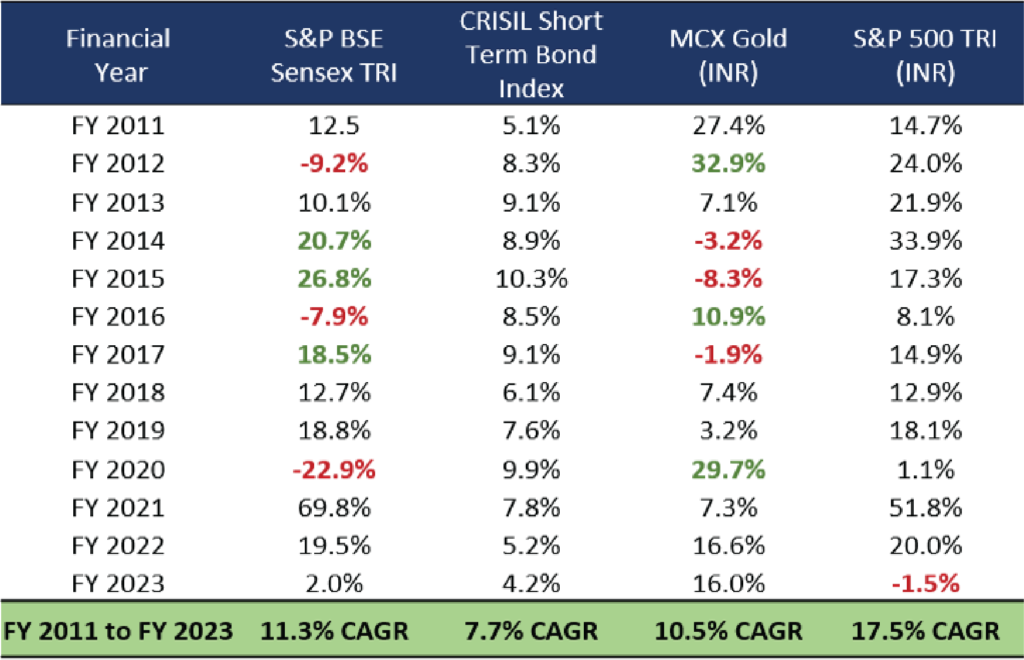

Financial Year wise performance (% return) of select indices

For example, In FY 12 and FY 20, equity contributed negatively, but gold sparkled. However,

regardless of these asset classes, fixed income provided stability to the portfolio.

In FY 15 and FY 17, equity performed well while gold corrected. Fixed income, on the other hand, remained isolated from the volatility of these assets.

Hence, a combination of these asset classes in a scientific way can be utilized to generate low volatility returns.

However , role of asset allocation is to manage and reduce risk, while alpha generation is dependent purely on bottom up security selection

What kind of shift is required to the overall portfolio?

To improve the overall portfolio return, it is evident that shifting some allocation from the traditional personal risk bucket to strategies like multi-asset allocation can be beneficial. Also with current tax lows debt mutual funds are now going to be taxed at marginal tax rate without indexation benefit, hence multi asset strategies with minimum 35% gross domestic equity makes a lot of sense. However, this shift should be done without altering the overall portfolio’s volatility too much.