Sec 80C of income tax is most popular section for Small & middle tax payers. Deduction is available only to Individual tax payer and HUF. Deduction available u/s 80C is Rs. 1, 50,000/- from Financial year 2014-15 (before it was Rs. 1, 00,000/-) to all assessees, means if Assessee is in 30% tax bracket than He/She can save Rs. 45000/- tax (30% of 1,50,000).

Sec 80C of income tax is most popular section for Small & middle tax payers. Deduction is available only to Individual tax payer and HUF. Deduction available u/s 80C is Rs. 1, 50,000/- from Financial year 2014-15 (before it was Rs. 1, 00,000/-) to all assessees, means if Assessee is in 30% tax bracket than He/She can save Rs. 45000/- tax (30% of 1,50,000).

Let us discuss deductions in brief.

Life Insurance Premium

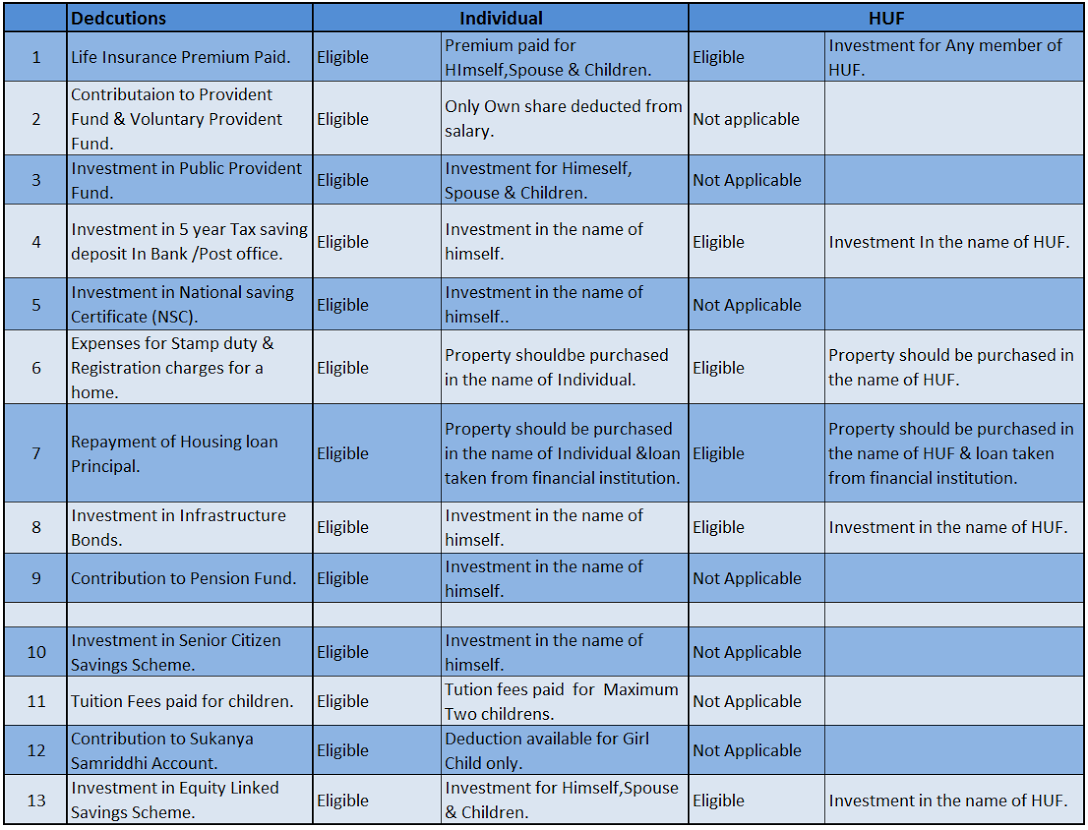

In case of Individual –

Individual can claim deduction for life insurance premium paid for himself, spouse and children (dependent or independent) but deduction not available for Premium paid for parent’s life insurance policy. If individual has more than one life insurance policy than deduction available to aggregate of all premium paid. It is not necessary to have the insurance policy from Life Insurance Corporation (LIC) – even insurance bought from private players can be considered here.

In case of HUF-

Individual can claim deduction for life insurance premium paid for members.

Provident Fund & Voluntary Provident Fund

Amount deducted from salary and deposited in Provident fund by employer (in case of salaried person) than it is considered to be investment and it is deductible u/s 80C .

Assessee has option to contribute additional amount through Voluntary provident fund and it is also considered as investment and deductible u/s 80C.

Public Provident Fund

In case of Individual-

Assessee can claim deduction of Amount deposited in PPF A/C of himself, wife and children’s (dependent &independent). PPF interest is exempt from tax and maturity amount is also exempt from tax so it is one of good investment scheme.

In case of HUF-

HUF can claim deduction of Amount deposited if PPF A/c of members.

5 Year Fixed Deposit & 5 Year Post office time deposit

Tax saving fixed deposit and post office time deposit of 5 year tenure is liable for deduction u/s 80C but interest earned on it is fully taxable. There are special fixed deposits in the bank which have maturity period of 5 years and are eligible for deduction under section 80C. Similarly Post offices also have a 5 year time deposit scheme which is also eligible for deduction under section 80C.

National Savings Certificate (NSC) (VIII Issue):

NSC is a time-tested tax saving instrument with a maturity period of five Years. Presently, the interest is paid @ 8.10% p.a. on 5 year NSC.

Premature withdrawals are permitted only in specific circumstances such as death of the holder. Investments in NSC are eligible for a deduction of up to Rs 150,000 p.a. under Section 80C. Furthermore, the accrued interest which is deemed to be reinvested qualifies for deduction under Section 80C. However, the interest income is chargeable to tax in the year in which it accrues.

Stamp Duty and Registration Charges for a home:

This is not much known by the tax payers that the amount you pay as stamp duty when you buy a house and the amount you pay for the registration of the documents of the house can be claimed as deduction under section 80C in the year of purchase of the house.

Repayment of Housing loan Principal:

Deduction is available of Repayment of Principal Amount (not interest amount) of Home loan taken from specified financial institutions or entities like your employer a public limited company, central government or state government or board, corporation, university established by law. However in respect of loans taken from your relatives though you can claim deduction under Sec

tion 24b for interest, the deduction under Section 80 C for repayment is not available.

Deduction is available from Assesse has taken possession of property and if property sold within 5 year of possession than deduction claimed in earlier years is taxable in the year of property sold.

First time home buyers will get additional exemption of upto Rs. 50,000/- on interest paid for loans upto Rs. 35 lakhs with cost of home upto Rs. 50 lakhs but property should be purchased between 01/04/2016 to 31/03/2017 and loan to be sanctioned during this period only.

Infrastructure Bonds:

These are also popularly called Infra Bonds. These are issued by infrastructure companies, and not the government. The amount that you invest in these bonds can also be included in Sec 80C deductions.

Pension Funds – Section 80CCC :

This section – Sec 80CCC – stipulates that an investment in pension funds is eligible for deduction from your income. Section 80CCC investment limit is clubbed with the limit of Section 80C – it means that the total deduction available for 80CCC and 80C is Rs. 1.50 Lakh. This also means that your investment in pension funds up to Rs. 1.50 Lakh can be claimed as deduction u/s 80CCC. However, as mentioned earlier, the total deduction u/s 80C and 80CCC cannot exceed Rs. 1.50 Lakh.

Senior Citizen Savings Scheme 2004 (SCSS):

Amount deposited in SCSS is deductible u/s 80 C. The account may be opened by an individual, who has attained age of 60 years or above on the date of opening of the account. & who has attained the age 55 years or more but less than 60 years and has retired under a Voluntary Retirement Scheme or a Special Voluntary Retirement Scheme on the date of opening of the account within three months from the date of retirement. & No age limit for the retired personnel of Defense services provided they fulfill other specified conditions.

Education Expense:

Assessee can claim deduction of Tuition fees paid for Children’s education purpose (restricted to only 2 children’s) but educational institute must be in India and deduction is available for tuition fees only. So any amount paid as development charges, library charges are not deductible. Here tuition fees don’t mean that fees of private tuition classes.

Sukanya Samiriddhi Account:

Sukanya Samiriddhi Scheme Launched by Prime Minister Shri Narendra Modi on 22 January 2015 for a girl child. Any amount deposited in the Sukanya Samiriddhi Account is deductible u/s 80C. Interest earned on account is Tax free and Amount received at the time of maturity if also tax free. Interest rate is 9.1% for FY 2014-15 ,9.2% for FY 2015-16 and 8.6% for 2016-17. Minimum amount can be deposited in one year is Rs.1000/- and maximum amount can be deposited is Rs. 1,50,000/-.

Equity Linked Saving Scheme (ELSS):

ELSS of Mutual Funds are more popular since they are giving good returns in long run and lock in period is just 3 years which is shortest lock in period in saving based investment u/s 80C. In case of investment done by SIP than each SIP installment is treated as separate investment for lock in period purpose.

To conclude with section 80C is a very comprehensive section which offers deduction of Rs. 150000 in total for all above investments or expenses from income directly. Tax payers should understand all these investments and expenses and plan their finances accordingly to take full advantage of this section.