Gold is a favorite asset class for Indians. Generally in India gold is inherited from one generation to another and every time quantity keeps on increasing. In my practice, I regularly face the question from my clients and readers of my blog that whether we should invest in gold or not? Many investors also believe that gold has given better returns than equity in past. So this article is an effort to bring some clarity on whether gold is a good asset class for investment or not.

1

Gold as an Asset Class:

As an asset class gold falls in precious metal category which falls in commodities.Being a commodity, price of gold mainly depends upon demand and supply principle.Supply of gold increases slowly and gradually, it cannot be raised immediately.So, gold prices rise sharply whenever the demand of gold increases sharply. Similarly when demand of gold falls, prices fall or don’t move up for years and years.

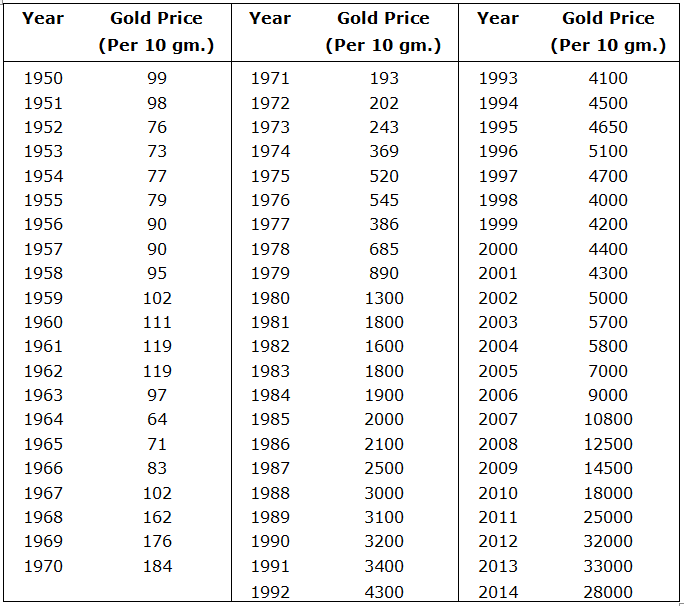

History of gold price:

Here in table below you can see the gold price history since 1950 per 10 gms.

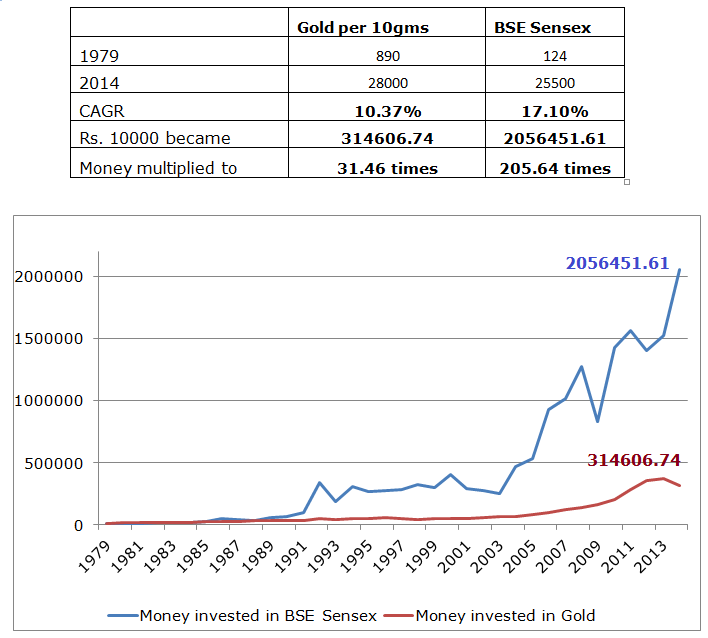

Investment in Equity Vs.Gold:

If we compare investment in equity vs. investment in gold, above Table and chart clearly indicates that between 1979 to 2014 gold price has grown from Rs. 890 to Rs. 28000 per 10 gms. Apparently this looks very high but when we calculate returns in compounded annualized terms it has given compounded annualized gross returns of around 10.37%, which is not very high. At the same time BSE Sensex has grown from 124 to 25500 between 1979 to 2014. This comes to a return of around 17.15% compounded annually. In above chart it is clearly evident that Rs. 10000 invested in Gold in 1979 became Rs.314606(31.46 times) whereas Rs. 10000 invested in BSE Sensex became Rs. 2056451(205.64 times). So it is very clear that equity is a better asset class than gold for long term investment.

Is gold really a safe heaven?

People invest in gold by thinking that gold is a safe heaven and gold prices will never fall. But this is not true. Gold prices can also fall and if you see above price history chart, there are years like 1967, 1976 and 2014 where gold prices have fallen. Another risk that gold carries is it does not beat inflation by heavy margin so over a long term it does not generate high real returns like equity. So for long term goals like retirement and Child’s education planning investors should not invest much in Gold.

When you invest in gold you also take risk of US Dollar:

Actually gold prices are calculated internationally in US dollar so whenever US Dollar appreciates against Indian Rupee, gold prices in India rises and vice versa. Due to this, between Oct-2012 to July- 2013, gold prices per ounce fell from 1794 US dollars to close to 1200 US dollars( approx. 30% fall) but during this time Indian rupee depreciated against dollar from around Rs. 55 to Rs. 70 per dollar so in India gold prices did not fall during this period. whenever you are investing in gold you are also affected by Rupee dollar relationship indirectly.

Should you invest in gold?

Before deciding on whether one should invest in gold or not, I want you to be very clear with your objective of why you are investing in gold? Are you investing in gold to accumulate it for marriage of your children or you are investing in gold as a part of your investment portfolio and want to generate return out of it, since both objectives need different approaches to handle.

Let us see in detail how to manage investment in gold for both these objectives individually.

1. How to accumulate Gold for Marriage:

If you want to accumulate gold for marriage of your children than you should start as early as possible and don’t wait for marriage years to come. In this scenario first of all you should decide how much gold will be required at the time of marriage of your child. And how many years are left for marriage of your child and spread this buying across this period. This is stated in below table.

As per above illustration suppose your Child’s current age is 9 years and approximate marriage age in your family and religion is 25 years then years left for marriage is 16 years. Now you need approx. 400 gms. Of gold for marriage so within next 16 years you have to accumulate 400 gms. of gold. My advice is to distribute it equally over next 16 years and buy 25 gms of gold every year. For this you can buy gold once a year on special occasions like, birth day of your child. In the years when gold prices fall, try to buy more than 25 gms so in years where gold prices rise sharply you can effort to buy less gold. This will help you in keeping your weighted avg. purchase price on lower side.

Now never sell this gold: – Never sell the gold that you have accumulated over the years, in order to make money or to trade on gold. Many times investors think that since gold is not required now so let me sell it and I will buy back when price will fall. This is a wrong approach. Always stick to your objective. Here your objective is not to make money but it is to accumulate gold for marriage.

2.How to accumulate Gold for investment purpose:

If you want to invest in gold for returns, decide a clear percentage allocation of your total portfolio to gold. You can give a percentage allocation to gold anywhere between 5% to 15% depending upon your circumstances. But don’t give much higher allocation to gold in your long term goals. Now simply try to maintain this allocation. What I mean is if you have given an allocation of 10% from your portfolio to gold than review your portfolio at regular periodic interval say every 6 months and if it has fallen below 10% than bring it back to 10% and if has gone beyond 10% than switch some money from gold to other asset classes which has fallen. This will help you to buy gold when prices have fallen or not moved up and sell gold when prices have increased sharply or other asset classes are available at cheaper rate.

Conclusion: Whenever you want to invest in gold, be clear with your objective of investing in gold. If you are buying gold for marriage purpose you can adopt above stated strategy and should not sell it or look at prices. But if you are buying it as a part of your investment portfolio than give a fixed percentage allocation of your portfolio and stick to it.

Also accept the fact that gold prices can also fall and over a long term there are very less chances that gold will beat equity returns. So for your long-term goals higher percentage allocation should not be given to gold.