Inflation is one of the biggest enemies in our financial life but most of the times I find that investors forget to consider impact of inflation on their financial lives. In this article I will try to explain “what is inflation?” from micro economic perspective and then we will see what is impact of inflation on our life?

What is Inflation?

As a general definition “Inflation is a continuous rise in the prices of commodities, goods and services.” This means that when prices of any goods, commodities or services keep increasing on a continuous basis that is inflation. But actually it is other way round, prices of commodities does not increase but value of currency keeps falling and that’s why its purchasing power also falls so what a 100 rupee currency note could buy a year ago, it cannot buy the same goods and services today. So there is fall in the value of rupee or purchasing power of rupee has fallen. There are many reasons for this but one primary reason for this is when the government prints new currency and puts in the economy by spending it on infrastructure, rising salaries etc. the value of existing currency falls. This happens because same commodities are chased by more currency. So Inflation is basically fall in the purchasing power of Rupee and not the rise in the price of the commodities.

How it affects your financial life?

The biggest mistake layman investors make is, they forget to consider impact of inflation on their financial life. Inflation has a severe impact on our long term goals like Retirement, Education Cost of our children etc. Let me explain you with few real life case studies to bring more clarity.

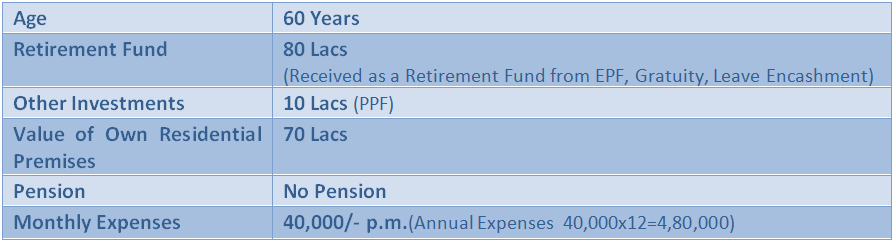

Recently, a client approached me for his financial planning. He had just retired from senior management of a very good company.

Following are his facts and figures.

This gentleman had saved in PPF and EPF for entire life except for some small life insurance policies. When I met him He was of the view that he has around 80 lacs corpus which is sufficient to survive. He told me that he will receive around 8% interest in fixed deposit which will come to

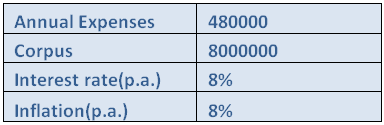

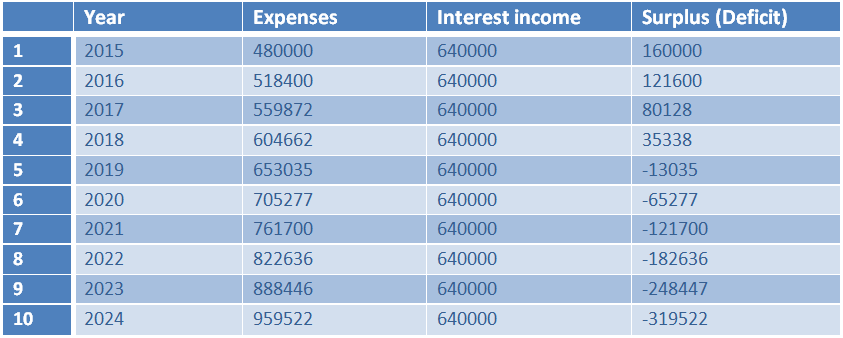

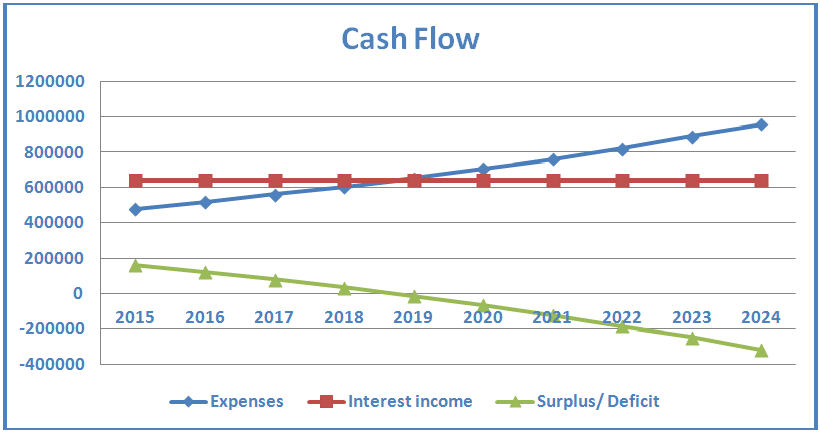

Rs. 640000 ( 8% * 8000000). His monthly expenses including all type of expenses are Rs. 40000 so annually he needs Rs. 480000/- and his interest income will be Rs. 640000 so he will save around Rs. 160000(640000-480000). In this case if I assume 8% p.a. inflation in his cost of living let us see How his annual cost of living increases over next 10 years.

For convenience we have assumed zero taxes and 8% interest rates. PPF corpus of Rs. 10 lacs is kept for meeting any medical emergencies and hence not taken into account in calculations.

Look in above table, in fifth year (2019) his cost of living is more than his interest income. Please note that he is not increasing his lifestyle, he is just maintaining his life style and from 2019 onwards if he wants to maintain same lifestyle, he will have to withdraw from his basic capital Rs. 80 lacs.

Mistake this gentleman made is he did not consider impact of inflation on his cost of living. Similarly let us see some other life goals how they are affected by inflation.

How inflation affects your Children’s education goals?

Last month a couple came to me to plan higher education cost of their one year old son. He estimated that his son will need Rs.20 lacs to go abroad to get higher education in a good engineering college when he reaches age of 17 years so wanted to invest from now. He wanted to invest Rs. 5 lacs now and believed that it will become Rs. 20 lacs when his son reaches 18 years. But this Rs. 20 lacs was today’s value of that education cost. When I asked about inflation on that cost he was blank and had no answer. Following table will show the inflation adjusted value of Rs. 20 lacs after 17 years.

The value of Rs. 20 lacs becomes Rs. 74 lacs after 17 years. So goal which was looking easy to achieve now looks very difficult.

When I made above calculation and showed him that inflation adjusted value of Rs. 20 Lacs will be around 74 lacs they were first shocked and argued that there is some mistake in calculation. Afterwards they accepted this calculation.

So inflation is our biggest enemy in completing our long term goals. But major issue is that while planning our future goals like Retirement, Education fund for our children etc. we don’t take into consideration inflation. Either we consider same level of expenses in long term or we don’t calculate their future values putting inflation percentage properly. This way inflation is the biggest risk to our long term goals but it has very low affect on our short term goals. Suppose a goal is only one year away from now then the inflation will not affect if much but for long term goals inflation is the biggest risk.

In my next article I will be writing on “How to fight with inflation?” and that will be in continuation to this article based on case studies discussed above.