In my first article on HUF & Tax Planning which was published on 4th June, 2015 I had discussed ” What is HUF? & How to create HUF?“ and in my second article on HUF & Tax Planning which was published on 19th June, 2015 I had discussed “How to reduce Tax Liability using HUF?“. In this article I have discussed other legal aspects of HUF & Disadvantages of HUF.

Legal Aspects of HUF:

Rights on Income & assets of the HUF:

HUF property and income are considered to be property and income of joint family and not of karta. So karta as a signing authority becomes manager of the joint family assets and income but he does not become owner of the joint family property.

Coparceners and Member of HUF : What is the difference?

Coparceners are those members which have become members of the HUF by birth. So all the coparceners are members but all the members are not coparceners. Wife becomes member by marriage so she is only member of HUF and she is not coparceners of HUF.

Is married daughter considered coparceners of HUF?

Yes, Daughters even after they get married are considered as coparceners of the HUF and have equal rights w.e.f. 09/09/2005 under Indian Succession Act, 2005.

Can there be all female HUF?

Yes, where a couple has only daughter and husband passes away, mother and daughter both can continue HUF.

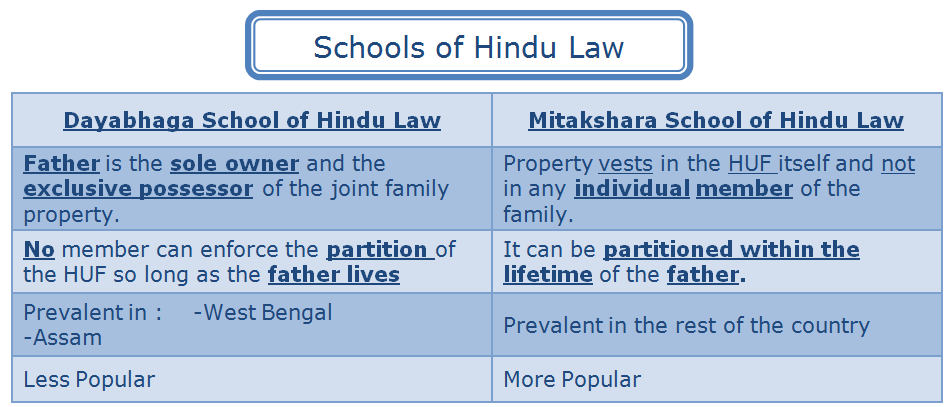

Two basic types of HUF:

Dayabaga and mitakshara.

Who can become Karta of HUF ?

The senior most male coparceners of the family can become Karta. Like in case of my father’s family, he is karta and HUF consists of my father, mother, my sister me, my wife and my children. But in case of my family I am the Karta and my family consist of me, my wife and my children.

In absence of senior most coparceners, due to his death or inability to manage due to any other reasons, the junior male member can also become Karta.

Can a female member become Karta?

In case of death of senior most male member, if all the male members are minor or there are no male members, female member can become Karta of HUF.

Partition of HUF: Partition of Hindu Undivided Family can be Total or Partial.

Total Partition: In case of Total Partition, all the members of HUF cease to be members and all the property of HUF cease to be property of HUF.

Partial Partition: In case of Partial partition, it can be partial vis-a-vis members, where some of the members separate out and others continue to remain part of HUF. It can be partial vis-a-vis properties, where some of the properties are divided where as others continue to remain property of be HUF properties

Difference between partition under the Hindu Law and that under the Income-tax Act: – There is a difference between a partial partition under Hindu Law and a partial partition recognized under the Income-tax Act. Though the concept of partition is the same under Hindu and tax laws, in two respects, recognition of partition under tax laws differs from that under Hindu Law.

For recognition of partition under Hindu Law division of properties by metes and bounds is not necessary. However, for recognition of partition under tax laws, division of properties by metes and bounds is necessary. Again under Hindu Law partial partition is recognized. However, in view of provisions of S.171(9) of Income-tax Act, 1961, partial partitions will not be recognized for tax purposes.

Right to claim Partition: – Under the Hindu law, any coparceners can make a claim for partition. This means that a wife cannot claim partition because she is a member but not coparceners of HUF. A member who becomes member of HUF by birth is only coparceners of the family. Whereas wife has become member of HUF by marriage and not birth.

Disadvantages:

Property once transferred to HUF cannot be converted to Individual: Property which is once converted to HUF property or any other income which is generated from HUF property will become HUF property and

cannot be converted to individual property of Karta or members without partition.This is very important because HUF property is a joint family property and all the coparceners have rights in it. Even married daughters also have rights in HUF property.

HUF property is a family asset and Karta doesn’t have any Rights: Karta is only manager of HUF and has rights related to management of HUF assets but this doesn’t mean that he owns HUF assets. He is just manager of HUF property.

2 Comments