In my earlier article I had written on what is financial Planning and How it is beneficial to you? As mentioned in that article , financial planning approach has a clear well defined six step process to manage your financial life. This process is defined by Financial Planning Standards Board of India. Now every financial planner makes a few changes in this process as per his understanding and suitability. Here I have discussed the process that we follow at our organization.

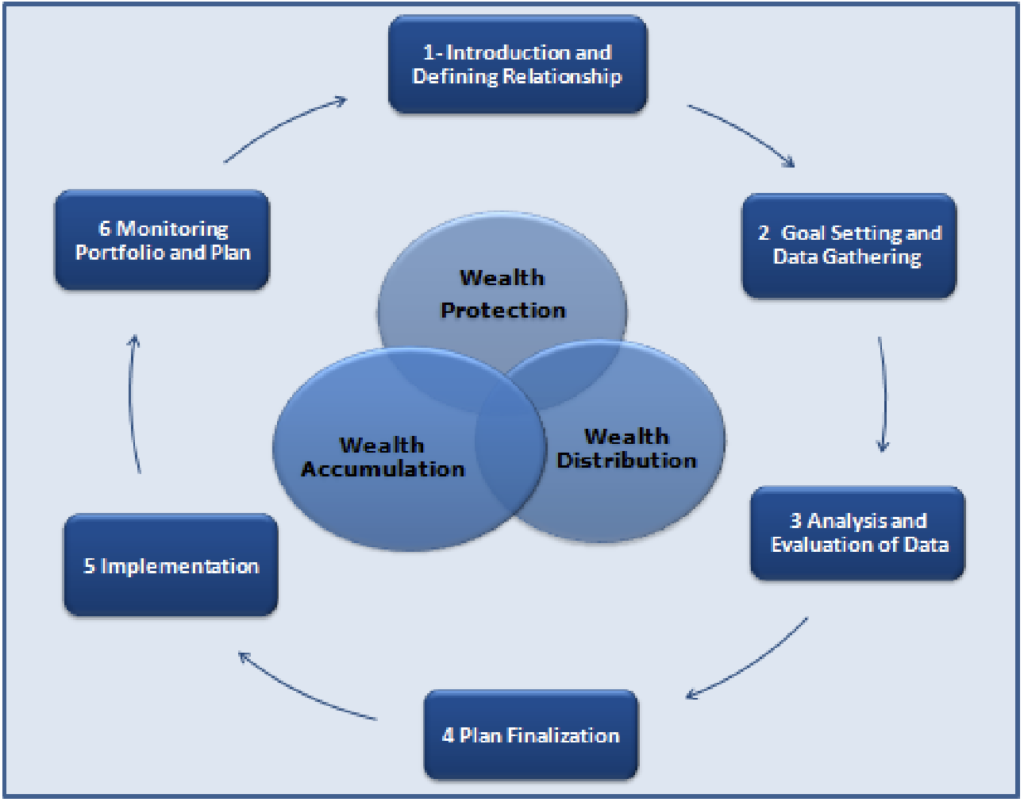

Step-1 Introduction and Defining Relationship:

This is a complementary meeting where financial planner introduces himself to the client and defines the relationship between client and financial planner. Here Financial planner defines his own roles and responsibilities, roles and responsibilities of client, what financial planning engagement will include, what financial planner can do for client and most importantly what financial planner can not do. This means it gives clarity to client what he should expect from this relationship and what he should not expect from this relationship. So, this step sets the platform for the long term relationship.

Step-2 Goal Setting and Data Gathering :

Once the client and planner agrees at the first step to go ahead, the second step is goal setting and data gathering. This step is the foundation for clients financial life. People who avoid systematic financial planning commit mainly two mistakes. First, is that they never set up clear goals for their financial life and second they never organize their financial data to bring it to one excel sheet or paper.

At this step planner sits with the client and his/her spouse and discuss what they want in their financial life? Here financial planner try to bring clarity in their minds regarding their financial goals and how they want to approach them. Once client is clear with his destinations (financial goals) it helps us(financial planner) to choose right direction and speed. After the goals are set planner will collect two types of data. First quantitative and other is qualitative. Quantitative data is regarding clients income, expenses, assets and liabilities. And qualitative data is related to his health related issues, his past experience with his investments, his approach towards money and other investments.

Step-3 Analysis and Evaluation of Data :

At this stage planner analyze clients data and try to do his SWOT(Strength, weakness, Opportunities, Threats) analysis. Here, at Ascent We make basic necessary assumptions and project his cash flow till his life expectancy (normally up to 90 year of life). Here planner analyze where the client stands right now and Where he wants to reach and with current level of income and investments what is the required rate of return to meet those goals. If client is not able to meet the goals next step is to do gap analysis and discuss with the client about prioritization of goals.

At this stage risk profiling of client is also done. Risk profiling is the process of deciding what percentage of client’s investment should be in aggressive asset classes like equity and real estate and what should be in conservative asset classes like bonds. Risk profiling helps to derive optimum risk level for the client. This mainly depends upon three factors, his ability to take risk, his need to take risk and his willingness to take the risk. Client’s ability and need are financial characteristics whereas his willingness is psychological characteristic.

Additionally here at our organization, we also educate clients with one or two coaching sessions as required regarding nature of different asset classes, what is asset allocation, how to manage risk, how compounding power affects his financial life and lot many things.

Step -4 Plan Finalization :

At this stage planner will finalize written financial plan. This basically is a road map for financial life of a client. Final written plan includes cash flow statement, contingency fund advice, Ratio analysis, asset allocation advice, Net worth analysis, Analysis of different goals and current achievement level, recommendation on insurance as well as investment.

Once financial plan is finalized, Planner also helps the client to finalize his succession plan through writing the will.

Step-5 Implementation :

Mere planning does not give any results. So at fifth stage implementation of the plan is carried on. All the steps are taken as per written financial plan which is customized to clients needs.

Step -6 Monitoring Portfolio and Plan :

Here two types of monitoring is required. First is at portfolio level and second is at plan level.

Portfolio Review: At this stage portfolio is reviewed at a regular periodic interval. For our clients we review portfolio at least once a quarter. This includes review of asset allocation as well as performance review of financial products like mutual funds etc…. Also execution is happening as per the plan or not is taken care of.

Plan Review :What ever plan is made, needs to be reviewed every year. So at this stage planner sitting with the client reviews if there is any change in the circumstances of the client or basic assumptions, on the basis of which plan was made than corresponding changes in the plan should be made.

To conclude,Financial planning is process and not the objective, so as shown in the above image it continuously keeps working and tries to achieve wealth protection, wealth accumulation and wealth distribution for the client.

Now those who have not adopted financial planning approach, should ask themselves whether they doing all the steps like goal setting, analysis of their financial resources and portfolio review and plan review. If not then they should give a serious though where there financial life is moving? Will they be able to meet their financial objectives comfortably.