Most of us have taken Loans in our lives for one or other objectives but When I speak with people on whether one should borrow or not and whether debt is good or bad, I find that most of people are on either extremes, some believe that one should always borrow money for their needs whereas others believe that as far as possible one should not borrow and live within his means. Both these approaches are not correct all the times. One should try to bring a balance in his approach towards using borrowed money. Whether the debt is good or bad depends on many factors like the objective of debt, tax benefits on interest etc and cannot be determined on the basis on any one factor. Also there is no single answer that can be applied to everyone. The answer of this question changes from person to person and situation to situation. This article is an effort to bring clarity when a debt can be considered good and when it can be considered bad.

Borrowed money comes at additional cost: First of all we need to understand one thing that borrowed money comes at cost. When you borrow money you have to repay along with interest. This interest increases the cost of asset or objective for which it was borrowed.

When you borrow you consume your future income in present: Another point that you should understand is when you borrow and consume it for any purpose, you have to repay along with interest cost in future. So here you are consuming your future income in present.

Debt can be considered good or bad on following aspects.

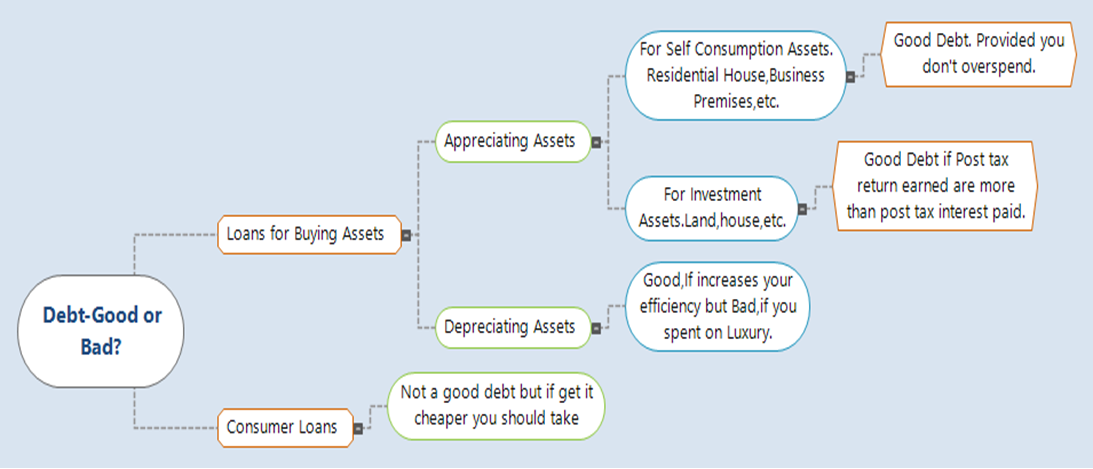

When it is taken to buy an Asset: Money can be borrowed to buy an asset. In such a situation it can be further classified in Appreciating Assets and Depreciating assets. Let us understand both the cases.

When it is taken to buy an Asset: Money can be borrowed to buy an asset. In such a situation it can be further classified in Appreciating Assets and Depreciating assets. Let us understand both the cases.

Appreciating Assets: Appreciating assets are the assets, the value of which will appreciate over a period of time. When loan is taken to buy any kind of property like home, land etc these are the assets for which value will generally appreciate. Please remember that in these assets also value can go down but mostly value will appreciate. Now such properties can be bought for self consumption like for residential purpose, business purpose or they can be bought for just investment purpose. Here I have given below my conclusion on both.

Properties for self consumption: When an asset is bought for self consumption like residential property or premises to run business the Debt (Loan) created to buy that property is good or bad should not be measured on appreciation of the property because it is for self consumption. Such property is taken for self consumption and that is why it is a good debt. But one should keep in mind that he is not over spending on that asset with borrowed money. For example if I need a 3 BHK flat and I buy a 5 BHK and spend a lot on decorating it with the borrowed money than it is not a good debt. This is because this type of property is bought for self consumption so how much it appreciates is not important but when you overspend on it, you have to pay significant cost for that borrowed money.

Properties bought for investment Purpose: When an appreciating asset like land, house etc are bought for investment purpose with borrowed money, it is good debt if it fetches you more post tax returns than post tax interest that you pay for the same. What I mean to say is that when you borrow money to buy a property for investment purpose, you are basically investing in real estate with borrowed capital so you have to earn more than your interest cost. While calculating your interest cost, you also have to consider tax benefit earned on that interest. So you have to give net effect of interest and similarly while calculating market value or sales value of your assets you have to consider tax to be paid on that.

If you are able to generate more post tax returns then it is a good debt otherwise it is not a good debt. But the problem here is it is difficult to guess returns at the time of buying such investment assets with borrowed capital. So in such a case you should be very conservative while taking such buying decisions. You should try to buy such assets at low valuations as far as possible.

Depreciating Assets: It is general belief that loans taken to buy depreciating assets are not good debts but this belief is not a true belief all the times. If a depreciating asset is bought to increase your working efficiency then it is a good debt. For example if you are buying a car or instruments for hospital with borrowed money, they are depreciating assets but they are going to increase your efficiency so it is not a bad debt.

In such case debt is bad when it is taken for depreciating assets which are luxury assets like if you need a car and you can easily do with a basic car which may cost you Rs.5 to 8 lakhs but you buy a luxury car of Rs. 15 lakhs then money borrowed for such luxury car is a Bad Debt according to me because here you are enjoying luxury at borrowed money.

Consumer Loans: Consumer loans are loans which are taken mostly for personal or family use. Like loans taken for buying small items of home use or travelling etc. ideally these loans increase your overall expenditure so they are not Good Debt but still if you get it at a lower or zero interest they are Good Debt.

Why should I borrow if I have my own resources to buy Appreciating assets, depreciating assets or consumer durables?

A question that comes from many readers is that why should I borrow for appreciating assets, depreciating assets or for consumer durables if I have my own resources. The answer is if you can earn more post tax returns on your own money than interest that you have to pay while borrowing that money than logically you should borrow rather than spending your own money. But while calculating interest to be paid please consider post tax interest if you are getting any tax advantage on that. Most of the investors forget to give tax impact on this.

Most of the people become emotional on this and believe that Debt is always bad and should use their own money when they have but this is not a rational decision so I would suggest you to use borrowed money in such cases.

Good Debt or Bad Deb is a Relative matter than Absolute: whether your Debt is good or Bad is a relative matter and cannot be judged absolutely on few factors. By relative I want to say that it is customized to once own circumstances like whether he gets tax benefit or not, he can earn better returns on his own money when he takes loan for something rather than investing his own money or not, so never try to take this decision just on the basis of a single factor that whether you are borrowing for appreciating asset or not, or whether you will get tax benefit on interest or not.

To conclude with borrowed capital is always at a cost so be very careful and calculative while using it and never take decisions on one or two factors alone.