Writing an article on financial planning for doctors is my favourite topic because 70% of my clients are doctors. During my practice I have worked with doctors from many different branches and with different age groups, like few of them are very young say between 32 to 35 years old and have just started their practice, few of them are at the middle of their career and at the age of around 42 to 50 and some are senior and close to their retirement.

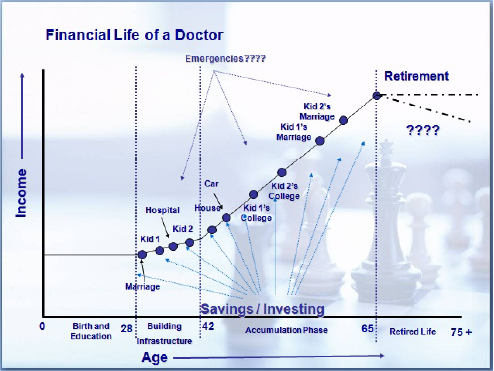

So from my experience I have understood one thing about doctors that their financial life is different than other professionals like lawyers, architect or entrepreneurs in many aspects like their career start very late, at the earlier stage of their career they are loaded with loans, strong cash flow starts only after 38 to 40 years, they cannot delegate their core work to others and are always running short of time. On the basis of my experience I would divide a doctors life into four stages as per the below graph.

Stage-1 Birth and Education: In case of a doctor, this stage normally ends at 28 years of age and till that time you are mainly dependent upon your parents for your financial needs.

Stage-2 Building Infrastructure: Once you start earning at around 28 years of stage your income starts and keeps growing. This is a stage where you build all the basic infrastructure for your practice like hospital, instrument and House along with the major events like marriage, kids etc. happening in your life. This stage normally continues till 42 to 45 years of age depending upon your branch. For some branches like Pediatrics or Dermatology, investment in instruments is relatively less whereas for some branches like orthopedics or cardiology, investment required in instruments is much higher. Here at this stage doctors also take many loans to set up infrastructure. A few points that I would like to make out for this stage which doctors should keep in mind are as following.

- Give priority to building hospital over house: Sometimes I have seen that as the income grows young doctors are more attracted towards building luxurious house and into that they delay hospital project or build smaller hospital. This is a wrong approach, once you decide to start your own practice, all your cash flow should be diverted to building a good and competitive hospital. When you delay your hospital project to build luxurious home, cost of the hospital project increases very fast and you also loose on income part and delay your practice by few years. Luxurious house can be built at a later stage also.

- Don’t invest in illiquid Investments: At this stage you should not put major part of your investments into illiquid investment avenues like PPF and Life insurance policies. In this stage of your life your practice expands at faster rate and medical practice has become a capital intensive profession nowadays. So if you invest major money in illiquid instruments it can sometimes create liquidity crisis for you and you may miss out some expansion opportunities. You should always have PPF account but at this stage but don’t invest too much in PPF account. More investment in PPF account should start once you complete your infrastructure building.

- Have maximum Insurance: This is the stage where you have maximum liabilities and less amount of wealth so if anything goes wrong with you, your family will have to suffer a lot. So take maximum life insurance and Disability insurance at this stage of your life. I have already written two articles in earlier editions of IMA monthly bulletin on this topic. I would recommend you to read these articles thoroughly. To calculate how much life insurance you need you can check the free calculator on our website http://bit.ly/fundazloo. Here I would once again say that always take online term life insurance plans and avoid taking insurance for investment purpose.

- Provide for Long Term Goals and avoid luxuries: The wealth that is accumulated at this stage will have maximum compounding cycles. So I would always recommend you to avoid some luxuries like cars and foreign trips at this stage to have fast wealth creation.

- Provide for Contingency Fund: At this stage you have significant cash outflow in terms of household expenses, Ms, regular expenses of your hospital etc. any small emergency like a small accident where you cannot work for a month or so may disturb your cash flow so you should provide at least six months of cash outflow as contingency fund and put it in your saving account or liquid investments.

Stage-3 Accumulation Phase: This stage normally starts between 42 to 45 years of age and continues till 65 year of age. At this stage normally liabilities are over or very less as compared to assets and income. At this stage cash flow is very strong so now a doctor should seriously start maximum accumulation for long term goals like retirement, children’s higher education etc.

- Reduce your Life Insurance: Normally my observation says that most of the doctors start taking bigger life insurance policies at this stage of life but actually as the assets grow and liabilities like children’s higher education and marriage gets over, you should reduce your insurance. Because once your liabilities are over or you have accumulated enough wealth to cover those goals you don’t need much insurance.

- Don’t avoid Retirement Planning: At this stage focus should be on providing for long term goals and mainly on retirement. Many times doctors argue that I will keep practicing for life time but at tater stage of your life your health may not permit you to continue with your practice or with the technological advancement you may not be able to compete with younger Doctors who have learnt latest technology. So Retirement planning is most avoided financial goals by the doctors which I don’t think is the right approach. At this stage you may see some major cash outflows for higher education of children and marriages of children, this will disturb your wealth accumulation so while spending on goals like marriages of children you should first provide for retirement because retirement is a goal which time wise comes last so many doctors keep spending on marriages and education excessively and then have to delay their retirement.

Stage-4 Retirement: Retirement is a stage where your regular income from primary source (practice or service) either slowly reduces or stops and you have to survive on the wealth accumulated during your working life. This is the most important stage of life because here your physical and mental health deteriorates slowly and you need maximum support from your financial assets. Nowadays we are living in the modern society so many times children are settled abroad or at some different place or even if they are in the same city you would not like to take their financial support at old age. So it is always better that you should provide for this stage from your young days.

- Wealth preservation and regular cash flow: During retirement stage wealth preservation should be given priority so you give priority over wealth accumulation. So your investments should be focused on bonds and other fixed income securities. Your investments should also be organized in such a manner that you have effective cash flow to meet your day to day needs have also provided for bigger medical emergencies.

- Succession planning: Succession planning is an important aspect of financial planning. Mostly we keep on avoiding this. I have written three articles on this in IMA monthly bulletin of earlier months. Ideally you should write your will at the earlier stage of your life but if you have missed that, I would recommend you to complete it here