In our previous newsletter, we discussed the fundamentals of succession planning, the role of a Will, and how a Private Family Trust can serve as an effective vehicle for preserving and transferring wealth. We also introduced the key parties involved and discussed why a Trust can be a more structured alternative to a Will.

Building on that foundation, this article takes a closer look at the structure of a Private Family Trust—its operational framework, the specific roles and responsibilities of each party, and how it differs from a Will in ensuring orderly, long-term wealth governance.

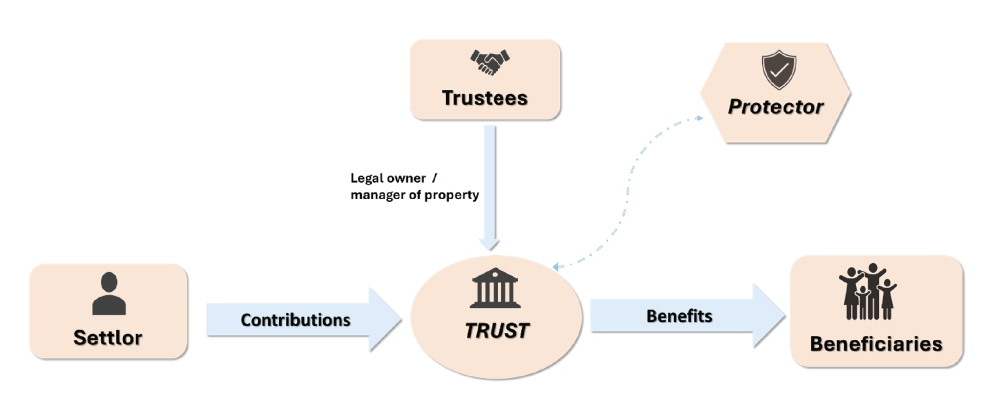

Trust Structure

The diagram above illustrates the fundamental architecture of a trust and the clearly defined roles that make it an effective long-term wealth planning tool.

At the starting point is the Settlor. The Settlor establishes the trust and contributes assets to it. These contributions form the trust corpus and are transferred with a clear intent—typically to ensure continuity, protection, and orderly distribution of wealth over time.

Once assets are contributed, they are held by the Trust, which acts as a separate legal structure. The trust does not operate independently; it functions strictly within the framework laid down in the trust deed, which governs how assets are managed and how benefits are distributed.

The Trustees are responsible for administering the trust. They receive authority from the trust deed to manage investments, oversee cash flows, and make distribution decisions. Importantly, trustees act in a fiduciary capacity, meaning they are legally and ethically bound to act in the best interests of the beneficiaries and in line with the Settlor’s intent.

The Protector, where appointed, provides an additional layer of oversight. While not involved in day-to-day operations, the Protector may be empowered to approve key decisions or intervene in exceptional circumstances, ensuring that the trust continues to function as originally envisaged.

Finally, the Beneficiaries are the individuals or entities for whose benefit the trust is created. They receive benefits from the trust in accordance with the terms set out in the trust deed—often in a structured and disciplined manner rather than as outright transfers.

Together, this structure creates a clear separation between contribution, control, oversight, and benefit-forming the foundation upon which a trust functions as a robust tool for succession planning, asset protection, and long-term wealth governance.

Operational Framework

Role of the Settlor

- The Settlor has no role in the ongoing operations or management of the trust once it is constituted.

- The Settlor appoints the original trustees and identifies the initial beneficiaries at the time of settlement.

- Any additional contributor to the trust assumes the role of a Settlor solely with respect to the contribution made, without acquiring operational control.

Duties & Powers of the Trustee

- To administer and operate the trust strictly in accordance with its stated objects and the trust deed.

- To buy, sell, and invest trust assets, and to monitor and manage investments on an ongoing basis.

- To distribute income and/or assets of the trust as provided under the trust deed.

- To claim reimbursement of reasonable expenses incurred in the course of executing trust objectives.

- To exercise all powers conferred by the trust deed in a fiduciary capacity and solely for the benefit of the beneficiaries.

Entitlement of Beneficiaries

- To receive benefits from the trust property in accordance with the provisions of the trust deed.

- To expect that trust assets are properly protected, administered, and applied by the trustees.

- In the case of a discretionary trust, to receive distributions of income or corpus as determined under the framework of the trust deed.

- The strength of a trust lies not in assets held, but in the structure that governs them. At its core, the framework brings structure and consistency to long-term wealth decisions.

How Trust is Different than Will ?

| Aspect | Will | Private Family Trust |

|---|---|---|

| When it operates | Only after death | During lifetime and beyond |

| Control | Complete control during lifetime | Oversight during lifetime / indirect control |

| Asset protection | Minimal | Strong |

| Susceptibility to disputes | High | Significantly reduced |

| Governance mechanism | None | Built-in |

| Suitable for | Simple estates | Complex, high-value estates |

| Beneficiaries | Can be anyone, even over relatives | Only relatives |

| Estate Duty Protection | None | Mitigation possible |

| Documentation | Flexible format, easy to prepare | Well drafted Trust Deed is required |