Basic Objective behind the Gold Schemes: From ancient times gold has been the favorite asset class for Indians and as a result of this we have been accumulating gold from generations and generations. I have never heard someone saying that as gold prices have gone very high I have sold a part of my holdings in gold or as gold prices can fall badly I am selling my holdings in gold. All the times I hear from readers or investors who participate in my programmes is that I buy this much amount of gold every year. An estimate says that Indians are having almost 20000 tonnes of idle gold lying with them either in their locker or at their homes. Value of this gold is estimated at around Rs. 55 Lakh crores. This gold is not traded nor monetized, on the contrary every year we keep buying new gold and add more to this gold holdings.

Basic Objective behind the Gold Schemes: From ancient times gold has been the favorite asset class for Indians and as a result of this we have been accumulating gold from generations and generations. I have never heard someone saying that as gold prices have gone very high I have sold a part of my holdings in gold or as gold prices can fall badly I am selling my holdings in gold. All the times I hear from readers or investors who participate in my programmes is that I buy this much amount of gold every year. An estimate says that Indians are having almost 20000 tonnes of idle gold lying with them either in their locker or at their homes. Value of this gold is estimated at around Rs. 55 Lakh crores. This gold is not traded nor monetized, on the contrary every year we keep buying new gold and add more to this gold holdings.

Basically we are a gold importing country and when we import Gold we have to pay in dollars and this affects our foreign exchange reserves adversely. So to reduce this and utilize the gold lying idle with households in India, Govt. Has decided to bring three different schemes in the country. These three schemes are Gold Monetization Schemes, Gold Sovereign Bond Scheme and Gold Coin & Bullion Scheme.

In this article I will be discussing Gold Monetization Scheme.

Basic concept of the Scheme: Gold Monetization Scheme was proposed in the 2015-16 Union Budget so that Idle gold assets can be mobilized and now it is approved. Let us see the features of the scheme.

Primarily Gold monetization schemes are about depositing idle gold assets by Resident Indians to banks in the melted form through Gold Saving Account. These deposits are for predefined period and will get an additional interest as offered by the banks. On maturity they have an option to get principle plus interest accrued in the form of gold or rupees, equivalent to accumulated interest plus principle on the price of gold prevailing on the date of maturity. This will assure that the person who is depositing his gold under this scheme with the bank will not miss the price movement in the gold price in the period of deposit and will also earn some interest on that gold deposit.

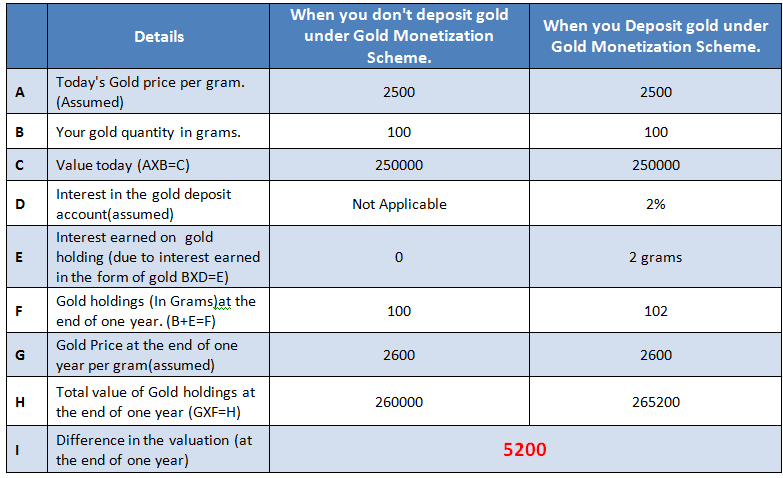

For example, if the bank is offering 1% interest and someone deposits 100 gms of gold for one year in Gold deposit account with that bank. After one year his account will be credited with 101 grams of maturity value (100 gram principle + 1 gram(1% interest)), now he has an option to get this maturity value of 101 grams either in the form of rupees equivalent to the price of the gold or in the form of physical gold. So he will not miss the appreciation (or fall ) in the price of gold and will also earn 1% gold as interest on that. On the other side if he keeps that gold with himself and doesn’t deposit under this scheme he will not be able to earn that 1% interest in the form of gold and have only appreciation ( or fall) in the gold price. This is shown in below chart.

It is clearly visible from above table that when idle gold is deposited under the scheme it earns additional gold and the valuation increases due to rise in price of gold plus rise in quantity due to interest earned under the gold monetization scheme.

I find people with large quantity of idle gold holdings with them which goes in kilograms. The returns generated on that will be significantly high if they use this scheme. Also this will be a service to country in a way that it will reduce gold imports and help the govt managing current account deficit.

Let us see the scheme in detail.

Process for Depositing in Gold Monetization Scheme: Following is the exact process that one has to follow for availing the benefits of Gold Monetization scheme.

Step-1 Purity Testing and Deposit of Gold:

At first step, depositor has to approach Hallmarking Centres which are certified by the Bureau of Indian Standards (BIS). These centres are engaged in certifying purity of the gold on a daily basis at prescribed fees. There are around 350 such centres across the country. They will conduct purity test in two parts as under.

Preliminary Test: Under Preliminary test, a preliminary XRF machine-test will be conducted to tell the customer the approximate amount of pure gold. If the customer agrees, he will have to fill-up a Bank/KYC form and give his consent for melting the gold. If the customer does not agree to the XRF machine test, he can take his jewellery back at this stage. The time spent by the customer will be about 45 minutes in the centre up till this stage.

Fire Assay Test: Once the customer agrees to go ahead for melting the gold, a further test of purity will be carried on at the same centre. For this, gold ornament will then be cleaned of its dirt, studs, meena etc. The studs will be handed-over to the customer there itself. Net weight of the jewellery will be taken after such removals and told to the customer. Then, right in front of the customer the jewellery will be melted and through a fire assay, its purity will be ascertained. These centres have viewing galleries from where the customer can see the entire process. The time taken is expected not to exceed 3-4 hours.

Deposit of Gold: When the results of the fire assay are told to the customer, he has a choice of either refusing to accept, in which case he can take back the melted gold in the form of gold bars, after paying a nominal fee to that centre; or he may agree to deposit his gold (in which case the fee will be paid by the bank). If the customer agrees to deposit the gold, then he will be given a certificate by the collection centre certifying the amount and purity of the deposited gold.

Step-2 Opening of Gold Savings Account: Once the customer has gone through purity test and deposited the gold with Purity Testing Centre and got the certificate for purity and amount of gold deposited, he has to come to banks for opening Gold Saving Account.

When the customer produces the certificate of gold deposited at the Purity Testing Centre, the bank will in turn open a ‘Gold Savings Account’ for the customer and credit the ‘quantity’ of gold into the customer’s account. Simultaneously, the Purity Verification Centre will also inform the bank about the deposit made.

Step-3 Maturity of Gold Savings Account: In case of Short Term Bank Deposits as mentioned below in this article, on maturity of Gold savings account, the customer will have option to get the maturity value( Quantity of gold deposited + interest accumulated on that ) in the form of physical gold or in the form of rupees calculated based on that days price of Gold. But the option has to be exercised at the beginning itself and option once exercised cannot be changed afterwards.

For Medium & Long Term Deposits, maturity calculation of maturity value will be as above but maturity will be paid only in Indian Rupee equivalent of the value of the gold and accumulated interest as per the price of gold prevailing at the time of redemption.

Other Important Aspects:

Who can opt for the scheme?

Any Resident Indians (Individuals, HUFs, Trusts including Mutual Funds/Exchange Traded Funds registered under SEBI (Mutual Fund) Regulations and Companies) can make deposits under the scheme. Joint deposits of two or more eligible depositors are also allowed under the scheme and the deposit in such case shall be credited to the joint deposit account opened in the name of such depositors.

This means that Non Resident Indians are not eligible for this scheme.

Minimum Deposit of Gold: The minimum deposit at any one time shall be 30 grams of raw gold (bars, coins, jewellery excluding stones and other metals).

Maximum Deposit of Gold: There is no maximum limit for deposit of Gold under the scheme.

Tenure of the Deposits: As per RBI circular, for this purpose scheme is divided in two parts.

(1) Short Term Bank Deposits and

(2) Medium and Long Term Government Deposit.

1) Short Term Banks Deposits : Theses deposit will be made with the designated banks for a short term period of 1-3 years (with a roll over in multiples of one year) . These deposits can be renewed with a rollover of 1 year.

(2) Medium and Long Term Government Deposit.: The deposit under this category will be accepted by the designated banks on behalf of the Central Government. These deposits will be accepted for a medium term of 5 to 7 years & long term 12 to 15 years.

Interest on Gold Deposits:

- Interest on deposits under the scheme will start accruing from the date of conversion of gold deposited into tradable gold bars after refinement or 30 days after the receipt of gold at the Collection & Purity Centre or the bank’s designated branch, as the case may be, whichever is earlier.

- In case of Short term Bank Deposits as mentioned above Interest rate will be decided by the banks and in case of Medium and Long Term Government Deposits, interest rate will be decided by the Central Government.

- In case of Short term Bank Deposits as mentioned above, both principal and interest to be paid to the depositors of gold, will be ‘valued’ in gold. For example if a customer deposits 100 gms of gold and gets 1 per cent interest, then, on maturity he has a credit of 101 gms.

Tax Treatment: As per original circular by Govt. Of India, this scheme will replace the earlier Gold Deposit Scheme, 1999 and interest earned under this scheme and capital gains will also be exempt from tax just like Gold Deposit Scheme, 1999.

Apparent Disadvantages of the schemes : following are few disadvantages of the schemes.

Melted jewellery: The major disadvantage is that we Indians hold most of our gold holdings in the form of jewellery and we are emotionally attached to this jewellery, not in case of Gold Monetization Scheme, if one wants to deposit the jewellery, then it has to be melted. This may not be acceptable to people in India.

Taxation Issue: Majority of the jewellery and gold lying with Indians is bought in marriages in cash or is inherited from our parents and grandparents, so most of us don’t have the proofs like bills etc. so if someone goes and deposits say 1000 grams of gold jewellery then he may have fear that income tax department will ask a question about when he bought this and about the source of jewellery. This is also major hurdle in this scheme.

Conclusion: To conclude with, if one has additional gold which he don’t want to use then the scheme can generate additional returns on that gold. Govt. has not taken enough steps to make the scheme popular and few practical hurdles like melting of jewellary and taxation problems have kept the scheme in silent mode.