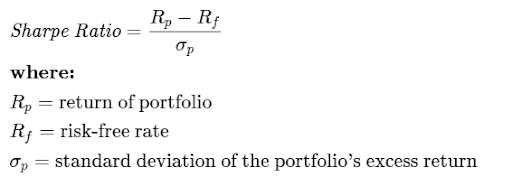

What is the Sharpe Ratio?

The Sharpe Ratio evaluates an investment’s return compared to its risk. It does this by measuring the excess return over a risk-free asset, like government bonds. A higher ratio indicates better risk-adjusted performance. It helps investors determine if higher returns justify the added risk.

An easy way to understand this is by thinking about a road trip:

- Portfolio Return (Rp) – This is like the distance you travel. Just as you want to cover more ground, investors want higher returns.

- Risk-Free Rate (Rf) – Think of this as the highway speed limit—a safe, predictable speed (like government bonds) that carries less risk.

- Standard deviation (σp) – Standard deviation shows how much an investment’s returns move up and down over time. A higher value means more unpredictability, while a lower one indicates stability. Imagine a road trip—smooth highways reflect low standard deviation (steady returns), while traffic and detours reflect high standard deviation (volatile returns).

Interpreting the Sharpe Ratio

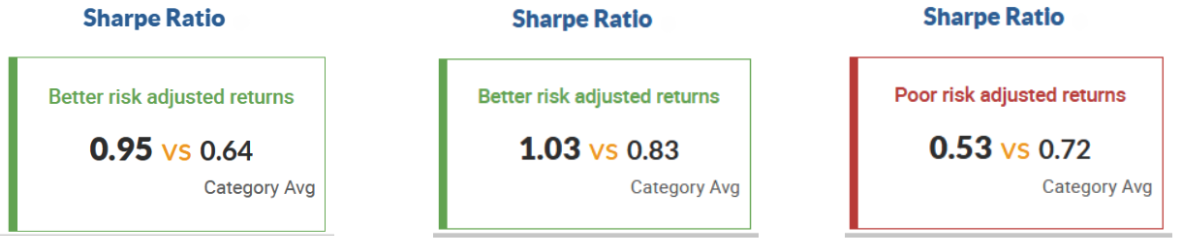

Sharpe ratios above 1 are typically seen as favorable, indicating that the investment delivers excess returns relative to its risk. However, investors don’t just look at a single number—they compare a portfolio’s Sharpe ratio to similar funds or market benchmarks. For instance, a portfolio with a Sharpe ratio of 1 may seem unfavorable if competing investments in the same category have ratios above 1.2.

Below is the Sharpe ratio comparison for large-cap, mid-cap, and small-cap mutual, presented without mentioning specific fund houses name.

Ratios calculated on daily returns for last 3 years (Updated as on 30th April, 2025)