In the ever-evolving world of money and aspirations, mutual funds have quietly become a trusted companion for the modern investor. They help people turn small, regular savings into meaningful long-term wealth by investing in a carefully selected mix of stocks, bonds, and other assets. With so many schemes available, one question often stands out: should you explore the potential of a newly launched New Fund Offering (NFO), or place your trust in an existing mutual fund with a strong and proven track record? This article walks you through the key differences between New Fund Offerings and existing schemes, helping you make informed decisions that align with your financial goals and long-term plans.

WHAT IS A NEW FUND OFFERING (NFO)?

A New Fund Offering (NFO) is the launch of a new mutual fund scheme by an Asset Management Company (AMC). During the NFO period, investors can subscribe to units of the fund at a fixed price, usually ₹10 per unit. This initial subscription phase allows the fund to raise capital and start building its portfolio.

NFOs are typically introduced to bring fresh investment themes or strategies to the market, such as funds focused on emerging sectors like technology, infrastructure, or socially responsible investing (ESG). They also help AMCs expand their product range to meet evolving investor interests.

TYPES OF NEW FUND OFFERINGS (NFOS):

When an AMC launches a New Fund Offering, the scheme is usually classified as either open-ended or closed-ended, each with distinct features:

1. Open-Ended NFOs:

These funds allow investors to buy and sell units at any time after the NFO period ends. They offer high liquidity, as you can enter or exit the fund on any working day at the prevailing Net Asset Value (NAV). Open-ended funds are more popular among retail investors because of their flexibility and ease of access.

2. Closed-Ended NFOs:

Closed-ended funds have a fixed subscription period during the NFO, i.e units cannot be redeemed with the AMC until the fund matures (usually after 3 to 5 years). However, investors can sell them on the stock exchanges if the fund is listed. These funds generally focus on specific investment strategies and may offer less liquidity but sometimes have a fixed maturity date, appealing to investors with a defined investment horizon.

NFO VS EXISTING MUTUAL FUND:

When investing in mutual funds, a common question is whether to choose a New Fund Offering (NFO) or an existing mutual fund scheme. Both options come with their own set of features and limitations, and the right choice depends on your investment goals, risk tolerance, and the level of clarity and information you prefer before making a decision.

1. Track Record and Performance History

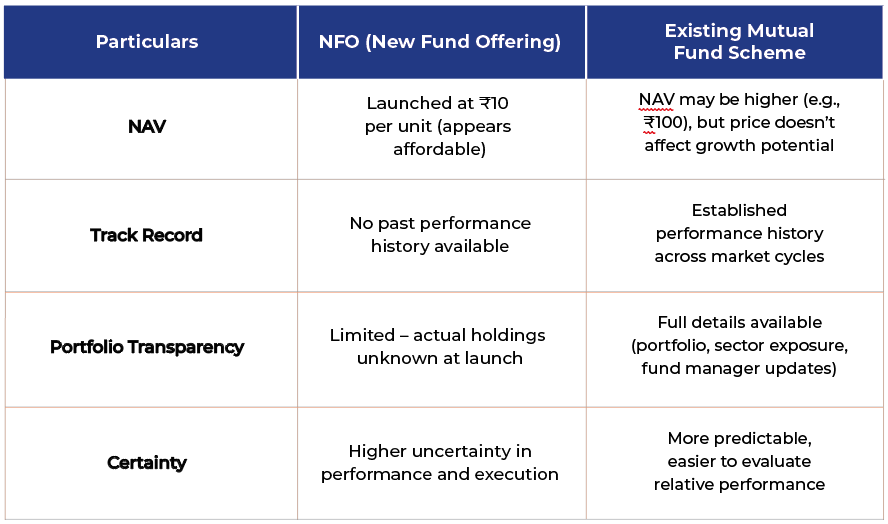

One of the most significant differences between an NFO and an existing mutual fund is the availability of performance data. An existing mutual fund has a track record, sometimes spanning several years that allows investors to evaluate how the fund has performed across different market conditions. You can analyze past returns, consistency, risk-adjusted performance (like Sharpe or Sortino ratio), and compare it with peers in the same category. In contrast, an NFO has no performance history. You're investing based on the fund’s investment objective, the fund manager’s reputation, and the credentials of the AMC. This makes it harder to judge the fund’s future potential, as there's no way to see how it has managed market ups and downs in the past.

2. Net Asset Value (NAV) and Pricing

NFOs are usually offered at a fixed price, typically ₹10 per unit during the launch period. This low price may seem attractive to some investors, giving the illusion of a “cheap” entry point. However, it’s important to understand that NAV is not a measure of value or potential returns. A fund with a NAV of ₹10 is not necessarily better than a fund with a NAV of ₹100. What matters more is how the underlying portfolio performs over time. Existing funds, on the other hand, will have a higher NAV if they have delivered returns over the years. While this might look “expensive” at first glance, it simply reflects the fund’s growth and performance and offers far more clarity than a newly launched fund.

3. Transparency and Portfolio Disclosure

With existing mutual funds, you have access to a wide range of data: past returns, portfolio holdings, sector allocations, fund manager commentary, risk metrics, and third-party ratings. This level of transparency helps you make a more data-driven investment decision. NFOs, on the other hand, offer very limited information at the time of launch. The portfolio is yet to be built, and while the fund's investment strategy is disclosed in the offer document, there is no way to see how those ideas will be executed in reality. As a result, investing in an NFO is a leap of faith to some extent.

4. Risk and Uncertainty

NFOs come with a higher level of uncertainty. Since there’s no historical data to evaluate, you’re relying entirely on future expectations. Even the fund manager might take time to deploy the capital and construct the portfolio. During this period, the fund could underperform, especially in volatile markets.

On the other hand, existing funds offer a much clearer picture of risk. You can assess how volatile the fund has been in the past, how it handled bear markets, and whether it meets your risk appetite and investment goals.

Here is a summary stating difference between NFO and existing scheme -

Things to Keep in Mind Before Investing in an NFO:

1. What’s the Fund’s Goal?

Make sure you understand what the fund aims to do and if it matches your investment needs and comfort with risk.

2. Who’s Managing the Fund?

Look into the fund manager’s experience and how well they have done with other funds in the past.

3. What Type of Fund Is It?

Find out if it’s an equity, debt, or hybrid fund and see if it fits well with your existing investments.

4 How Much Will It Cost?

Check the expense ratio—the fees charged by the fund. High fees can reduce your overall returns.

5 What’s Happening in the Market?

Think about how the market is doing right now because it can impact how well the fund performs.

Conclusion

Both NFOs and existing mutual funds have their own strengths. NFOs can be a good option if you're an experienced investor looking to explore new ideas. But for most investors, existing mutual funds are usually the safer and more reliable choice - thanks to their track record, transparency, and flexibility. The key is to choose what fits your goals, risk level, and how much information you’re comfortable with before investing. It is always advisable to consult your financial advisor before making. any investment decision.

1 Comment