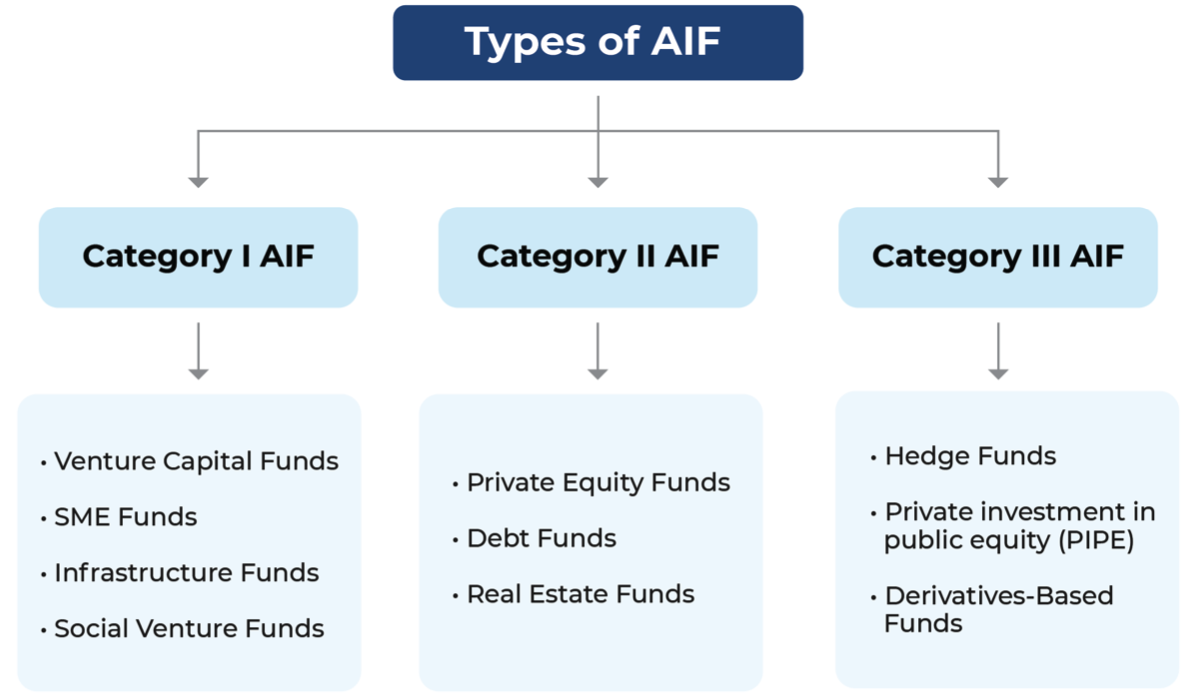

Categories of Alternative Investment Fund

Category I AIF –

- Category I Alternative Investment Funds aim to channel investments into sectors that support long-term economic growth and social welfare.

- These typically include start-ups, early-stage ventures, infrastructure projects, SME funds, social ventures funds focused on inclusive development.

- Because of their developmental role, the government often encourages them through tax benefits, regulatory support, or relaxed investment norms.

- Investors in Category I AIFS generally take a long-term view and are willing to accept higher risks in exchange for potentially substantial returns.

Category II AIF -

- Category II Alternative Investment Funds primarily invest in private businesses, debt instruments, and other structured strategies that do not fall under Category I or III.

- The target investments are companies with strong fundamentals that require capital for expansion, restructuring, or long-term growth.

- While these funds don’t benefit from specific regulatory incentives, they operate with greater flexibility and are subject to standard SEBI compliance.

- Various types of funds such as real estate funds, private equity funds (PE funds), fund of funds etc. are registered as Category II AIFs.

Category III AIF –

- Category III AIFS are designed for investors seeking high returns through complex and actively managed strategies.

- These funds can use leverage and invest in instruments like derivatives, structured credit, and arbitrage trades.

- Due to their high-risk nature, they are suitable only for experienced and well-informed investors.

- Funds registered under category III of AIF are, Private Investment in Public Equity Fund (PIPE Funds), hedge funds etc.

Understanding Taxation

Since the categories are different with different investment vehicles, the tax implications are also different for each of them. Let’s see the tax implication for each of them.

Taxation in the case of Category I & II -

Nature of Income Earned by AIF | Taxability | Who Pays Tax | Applicable Tax Rate |

|---|---|---|---|

Capital Gains (non-business income) | Pass-through* | Investor | LTCG: 12.5% STCG: 15% |

Other Income (e.g., interest, dividends) | Pass-through | Investor | Taxable as per investor’s tax slab. |

Business Income | Taxed at AIF level | AIF | AIF as LLP/Company: As per applicable tax rates. AIF as Trust: 42.744% (MMR). |

Dividend Distribution Tax (DDT) | Not applicable | N/A | No DDT liability on distribution |

TDS on Income (non-business) | 10% TDS deducted at source by AIF on income distribution | Deducted by AIF | 10% TDS (subject to applicable DTAA for non-residents) |

*Pass-through status – It means that the income or loss (other than business income) generated by the fund will be taxed at the hand of the investor and not by the fund business.

Taxation in the case of Category III -

- This category of funds is taxable at the fund level.

- There is no pass-through status.

- The highest rate of tax (as per the current tax slab) is charged on the profit made by this fund

- A Category III AIF pays tax on the following four types of income as per applicable tax rates-

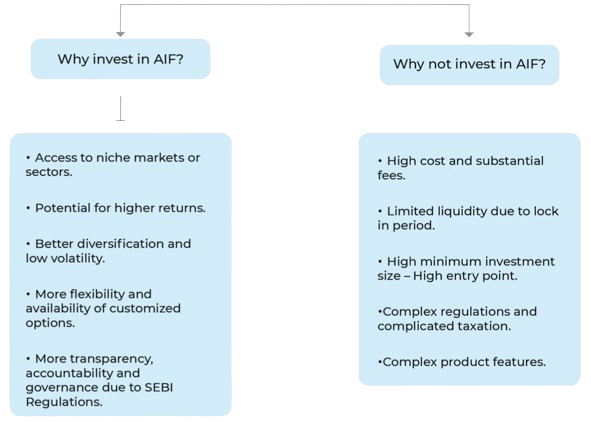

Why and why not invest in AIF?