In today’s increasingly globalized world, NRIs often find themselves straddling two financial ecosystems - one where they live and work, and the other back home in India. This dual exposure presents both opportunities and complexities when it comes to building and managing a long-term investment portfolio. The key to navigating this duality lies in smart asset allocation - the strategy of diversifying investments across various asset classes and geographies based on individual goals, time horizons, and risk tolerance.

Why Global-Indian

NRIs frequently have:

- Earnings and expenses abroad (e.g., UAE, US, UK).

- Emotional or financial ties to India, such as family obligations, real estate holdings, or future retirement plans.

- Currency exposure in both INR and their local foreign currency sometimes even in USD.

- Tax implications in both jurisdictions.

This makes it essential to design a well-thought-out asset allocation plan that not only ensures returns but also manages risks, taxes, and liquidity effectively. Nature of Financial Goal/ Future Cash Outflow is also to be considered.

Step 1: Define Your Financial Goals

Before allocating assets, clearly define your financial objectives:

- Short-Term: Buying an electronic appliance, children’s school fees, or a small vacation

- Medium-Term: Business investment, children’s higher education or marriage, buying a car

- Long-Term: Buying a House, retirement in India or abroad, legacy planning

Also, assess where each goal is to be met ie. in India or abroad, as this will influence the currency, taxation, and liquidity considerations.

Step 2: Decide the Allocation Between Indian and Global Assets

A simple framework NRIs can follow is to allocate assets based on the location of future liabilities:

| Type of Goal | Asset Location |

|---|---|

| Child’s US education | Global (US-based ETFs, MFs etc.) |

| Retirement in India | Indian assets (MFs, PMSs, FDs) |

| Short-term expenses in country of residence | Local bank deposits, USD liquidity funds |

Step 3: Choose the Right Asset Classes

Global Investments:

US/Global Equity ETFs (through well renowned and trusted platforms) International Mutual Funds (Feeder funds in India)

Bank deposits or fixed income in your resident country

Indian Investments:

Mutual Funds (via NRE/NRO accounts)

PMS (Portfolio Management Services) – Ideal for HNIs looking for alpha Fixed Deposits in NRE (tax-free) or NRO accounts

Real Estate (with rental income in INR)

Equity/Debt Instruments via Stock Market

Step 4: Currency and Taxation Considerations

Currency Risk:

An NRI saving in USD but investing in INR assets is exposed to INR depreciation. One must hedge this risk by diversifying globally or matching assets with liabilities in the same currency.

Taxation:

India: Gains on mutual funds, real estate, and FDs are taxable with TDS.

Abroad: Some countries like UAE have nil taxes, while the US taxes global income. Double Taxation Avoidance Agreements (DTAAs) can help reduce the burden.

Step 5: Monitor and Rebalance

Just like residents, NRIs must periodically review and rebalance their portfolio. Changes on various economical and personal fronts can impact the asset alloca- tion between Global and Indian investments, like:

Tax laws (in India or abroad) Residency status

Currency movements Status of Financial Goals Personal life stage

All impact the optimal asset mix. Rebalancing ensures that your portfolio doesn’t drift too far from your intended risk-return profile.

Although the core emphasis is on creating measurable social impact, these funds also aim to generate steady financial returns for investors.

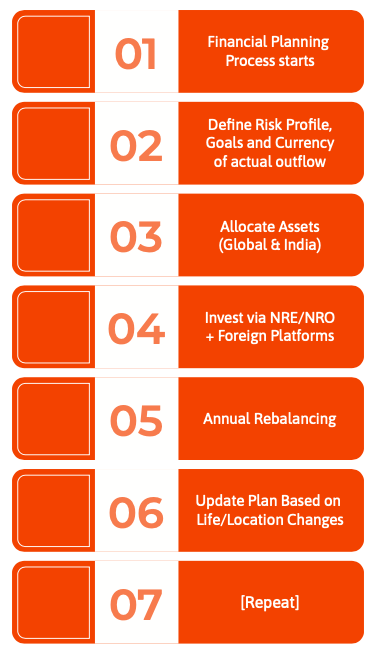

Here is how entire flowchart of above activity would look like.

Common Mistakes to Avoid

- Overexposure to Indian real estate without liquidity.

- Ignoring tax rules of home country on global income.

- No will or estate plan for Indian assets.

Underestimating repatriation complexities while changing the country of residence.

Disclaimer:

Asset allocation is not a one-time activity but an ongoing process. For NRIs, it involves an additional layer of complexity but also opportunity. With the right advisor and disciplined strategy, you can harness the best of both worlds - global and Indian - to achieve true financial freedom.