The Tax-Free Edge: Why UAE Investors Should Capitalize on Indian Markets

“If you have significant capital gains tax liability on eligible securities, shift to the UAE for more than 183 days. Your family holiday abroad will be funded from the savings on capital gains tax.” That is Kotak Mutual Fund MD Nilesh Shah’s take on how some of India’s wealthy are strategically managing their investments to minimize capital gains tax and maximize their returns.

In this article, let us discuss the capital gain taxation applicable to UAE residents, analyze key aspects of tax treaty between India and UAE and explore how strategic financial planning can help you retain most of your gains by reducing potential tax liabilities.

Tax-Free UAE vs Taxed India: A Quick Comparison

When it comes to personal income, the UAE stands out as a global tax haven. With no income tax on individuals, UAE residents get to keep every dirham they earn. Unlike many countries, there's no need to file annual tax returns or worry about tax brackets—making life simpler and finances more predictable for residents.

In contrast, earning in India comes with a tax bill. Individuals are taxed based on income slabs, with rates going up to 30% for higher earners—plus cess and surcharges in some cases. The system offers various deductions and exemptions, allowing individuals to optimize their tax outgo through smart financial planning.

How UAE residents can invest tax free in India?

In India, capital gains from the sale of listed securities and mutual fund units are subject to taxes at the rate of 12.5% for long-term gains for profits exceeding Rs. 1,25,000 and 20% for short-term gains. But if you are an UAE resident, believing in India’s growth story and investing here in Indian markets, the DTAA i.e. Double Taxation Avoidance Agreement between India and UAE has got you well protected, giving a distinct opportunity to grow your wealth tax-free. This agreement ensures that capital gains from sale of listed securities and mutual fund investments in India are not taxed twice – making India even more attractive investment destination.

What is DTAA?

DTAA stands for Double Tax Avoidance Agreement. It’s a tax treaty signed between two countries to ensure that individuals and companies don’t get taxed on the same income twice. It allows investors to claim relief from tax in their home country for the tax paid in the foreign country. India has signed 94 DTAAs with several countries, some of which include Australia, Austria, Bulgaria, Canada, UAE, Singapore, UK, Sri Lanka, etc.

Understanding DTAA between India & UAE

India UAE DTAA came into effect from 22nd September, 1993 and has been revised multiple times since then.

Article 2 of the Agreement talk about the existing taxes to which the Agreement apply. Taxes covered are as under

In UAE | In India |

Income Tax | Income Tax including surcharge |

Corporation Tax | Surtax |

Wealth Tax | Wealth tax |

Article 4 of the Agreement defines resident in case of UAE as: an individual who is present in UAE for 183 days or more in a calendar year concerned and a company which is incorporated in the UAE and which is managed and controlled wholly in UAE.

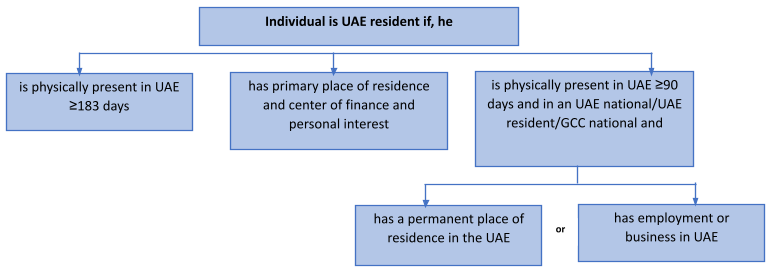

To dive deeper, a natural person will be considered a UAE tax resident if the individual meets any of the below mentioned conditions:

- Has one’s usual or primary place of residence and one’s centre of financial and personal interests in the United Arab Emirates.

- Was physically present in the United Arab Emirates for a period of 183 days or more during a consecutive 12-month period.

- Was physically present in the United Arab Emirates for a period of 90 days or more in a consecutive 12-month period and is a UAE national, holds a valid residence permit in the United Arab Emirates, or holds the nationality of any Gulf Cooperation Council (GCC) member state, where the individual:

- has a permanent place of residence in the United Arab Emirates, or

- carries on an employment or a business in the United Arab Emirates.

Alimony and Taxation: Key Rules to Understand

Article 13 also talk about taxability of following assets

Sr No | Type of Gain | Taxing Rights |

|---|---|---|

1 | Gains from sale of immovable property (as per Article 6(2)) located in the other Contracting State* | Taxable in the country where the property is located |

2 | Gains from sale of movable business assets of a permanent establishment or fixed base | Taxable in the country where the permanent establishment or base is located |

3 | Gains from sale of shares in companies whose assets mainly consist of immovable property | Taxable in the country where the immovable property is located |

4 | Gains from sale of other shares in a company resident in a Contracting State | Taxable in the country where the company is resident |

5 | Gains from sale of all other property not covered in clauses 1 to 4 | Taxable only in the country of the seller’s residence |

Clause 4 of Article 13 of the India-UAE DTAA covers capital gains arising from the sale of securities such as shares of listed company and Clause 5 being residual clause, gain from sale of securities such units of mutual fund. Under this provision, capital gains earned by UAE-based NRIs from sale of such securities in India are taxable exclusively in the UAE. Given that the UAE levies no personal income tax, these gains effectively remain tax-free for its residents—offering a significant advantage to UAE investors.

(*The terms "a Contracting State" and "the other Contracting State" mean U.A.E. or India as the context requires)

Requirements

The benefits of the DTAA can be extended to the NRIs upon submission of following documents:

- Tax Residency Certificate -

Also known as Tax Domicile certificate in UAE. Obtaining TRC from the country of residence is mandatory. While filing Income Tax Return in India as a non-resident, disclosure about TRC is must.

- Form 10F -

In case TRC does not cover all the details, such as nationality, tax identification number, address outside India, etc., such information will need to be filed electronically through Form 10F.

ITAT Ruling Backs Tax Relief for NRIs in Zero-Tax Countries

Recently, the Mumbai Income Tax Appellate Tribunal (ITAT) has ruled capital gains earned from Indian mutual fund units by NRIs will not be taxed in India. Its decision is based on the India-Singapore Double Taxation Avoidance Agreement (DTAA).

The ruling was given while hearing an appeal by Anushka Sanjay Shah, a Singapore-based NRI. (Anushka Sanjay Shah, Mumbai vs Income Tax Officer , Mumbai). Shah had earned Rs 1.35 crore in short-term capital gains from the sale of equity and debt mutual fund units during the assessment year 2022–23.

The ITAT judgment effectively makes capital gains from Indian mutual funds tax free for NRIs in countries like UAE and Singapore, which do not impose capital gains tax.

Conclusion

For UAE-based NRIs, the India-UAE DTAA opens the door to significant tax savings, especially on capital gains from Indian mutual funds and listed securities. With no capital gains tax in the UAE and favorable treaty provisions preventing double taxation, strategic investment planning can help maximize returns while minimizing tax liabilities. As recent rulings like the ITAT’s decision in the Anushka Sanjay Shah case reaffirm, India continues to be a promising destination for global investors—especially those from zero-tax jurisdictions like the UAE. By aligning your residency status and investment choices smartly, you not only participate in India’s growth story but also retain more of your hard-earned gains. However, it is advisable to seek professional opinion about investments as well as filing income tax returns.

(Sources – Income Tax India, Indian Kanoon, PWC Tax Summaries, Tax2Win)