Every other asset class caps your upside. A startup can return 1,000x — and that single outcome can outperform a lifetime of conventional investing. Four structural reasons explain why.

- Loss is capped. Gain is not.

In equities, real estate, or gold, your maximum loss is 100%, and your upside is bounded by market growth — a great Nifty stock might 5x over a decade. In a startup, the downside is identical: you lose your cheque. But the upside has no ceiling. When Info Edge put 4.7 crore into Zomato in 2010, the worst case was losing 4.7 crore. The actual outcome was a stake worth over 39,455 crore at IPO — more than 1,000x (Business Standard, 2021). No listed stock, property, or gold bar has ever replicated that arithmetic. - Price Discovery Advantage

You buy before the world knows the price. When you buy a listed stock, millions of analysts and institutions have already priced in the opportunity. When you back a seed-stage startup, you are setting the price — before revenues, before brand recognition, before market consensus forms. That information asymmetry is the engine of extraordinary returns. Accel Partners entered Flipkart when Indian e-commerce was barely a concept; by the time Walmart paid $20 billion+ for a majority stake in 2018, the category had been won. They did not get rich by being smarter than the market. They got in before the market existed. - Network Effect

Network effects build walls no competitor can scale. Zomato is more valuable today because more restaurants list on it, which draws more users, which attracts more restaurants — a self-reinforcing loop that compounds value non-linearly. Groww is stickier because a larger investor base deepens liquidity and lowers costs for everyone. Once a startup achieves that kind of scale, displacement is structurally difficult. That dynamic is simply unavailable in commodities, fixed income, or physical assets, where one unit of supply is interchangeable with any other. - Power Law Math

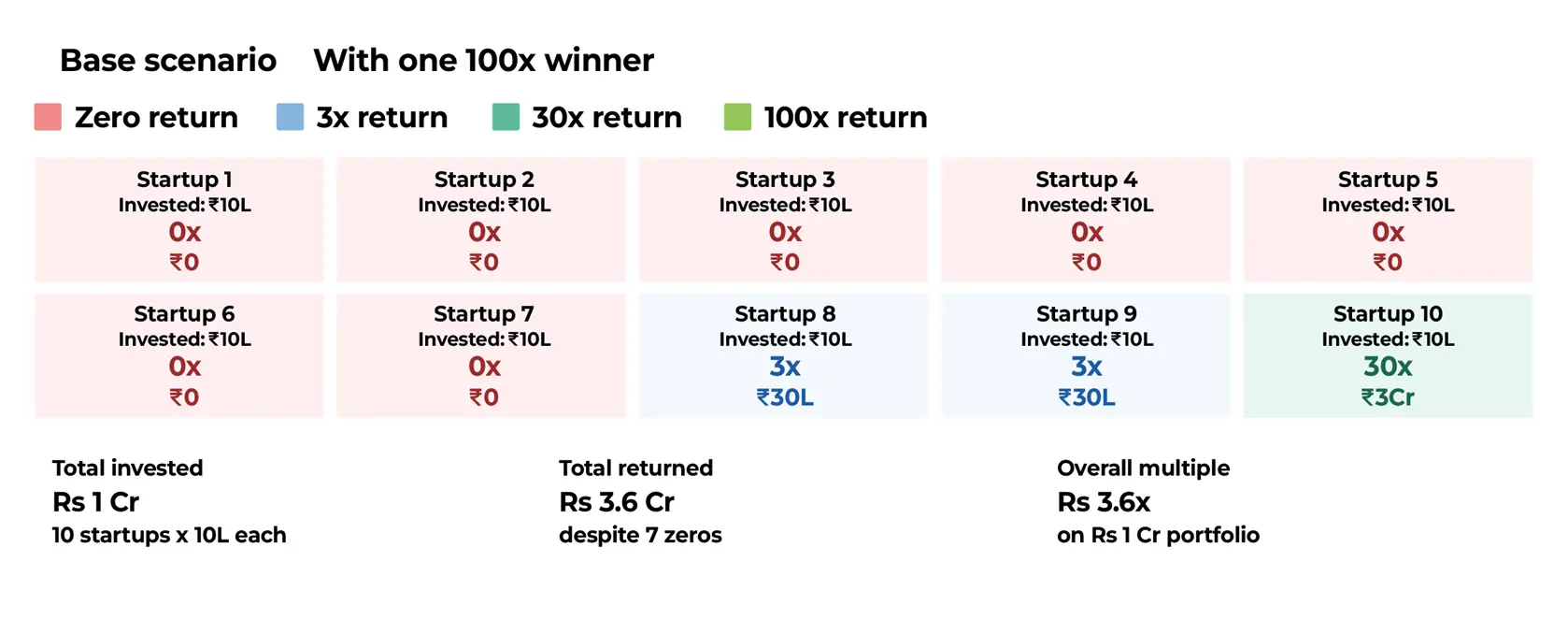

The power law means one conviction bet funds the whole portfolio. Venture math is unlike any other asset class. Consider a portfolio of 10 startups at 10 lakh each. Seven return zero, two return 3x, one returns 30x. Total return: 3.6 crore on X1 crore invested — a 3.6x return with a 70% failure rate. In no other asset class does that arithmetic work. And if that one outlier returns 100% instead, the portfolio delivers 10.6x.

In every other asset, time and compounding do the work — slowly. In startups, value creation is non-linear. A company solving a real problem at scale does not grow at 12% a year. It can grow 10x in three years and 10x again after that. That is why a single early-stage conviction bet, held patiently, can do more for a family’s long-term wealth than decades of disciplined saving in conventional markets.

Understanding where startup investing fits into a broader portfolio is essential before committing capital.

Appropriate allocation for HNIs (as a % of investable financial assets, excluding primary residence and operating business assets):

- Conservative: 3-5% in SEBI-registered AIF/VC funds only

- Moderate: 7-12% across a combination of VC funds, co-investments, and syndicates

- Aggressive: 15-20% for sophisticated investors with long horizons, strong deal flow access, and adequate liquidity buffers elsewhere.

The cardinal rule: never allocate capital you may need within seven to ten years. Startup investing is a long-duration asset class, and liquidity events rarely arrive on schedule.