When asked, “Have you planned your succession?”, most of the people respond with calm assurance — “Not yet. There’s still time.” Ironically, this assurance is often the first and most common mistake in personal wealth planning.

As wealth grows and families evolve across generations, the question is no longer about how wealth is created, but how it is preserves, protected and passed on meaningfully to next generation, without friction, fragmentation or family discord.

In this article, lets discuss what is Private Family Trust as a tool for succession planning, why it is needed and how it is different than will.

Will – a traditional tool for succession planning

Have you already thought about when succession planning should begin for your family, or is it something you’ve been meaning to revisit? If you’re comfortable sharing, tell us in the comments or write to us on celebratinglife@ascentsolutions.in

Private Family Trust – structured vehicle to plan succession

- Separate ownership from control

- Define clear rules for asset management and distribution

- Ensure continuity beyond individual lifetimes

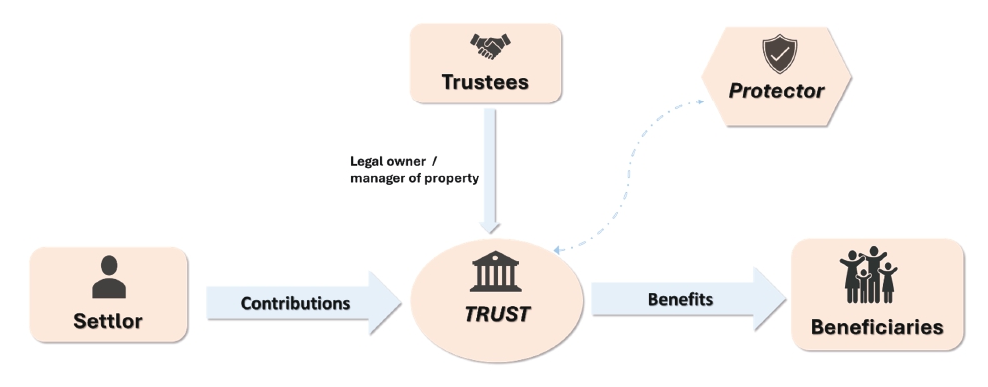

Trust Structure

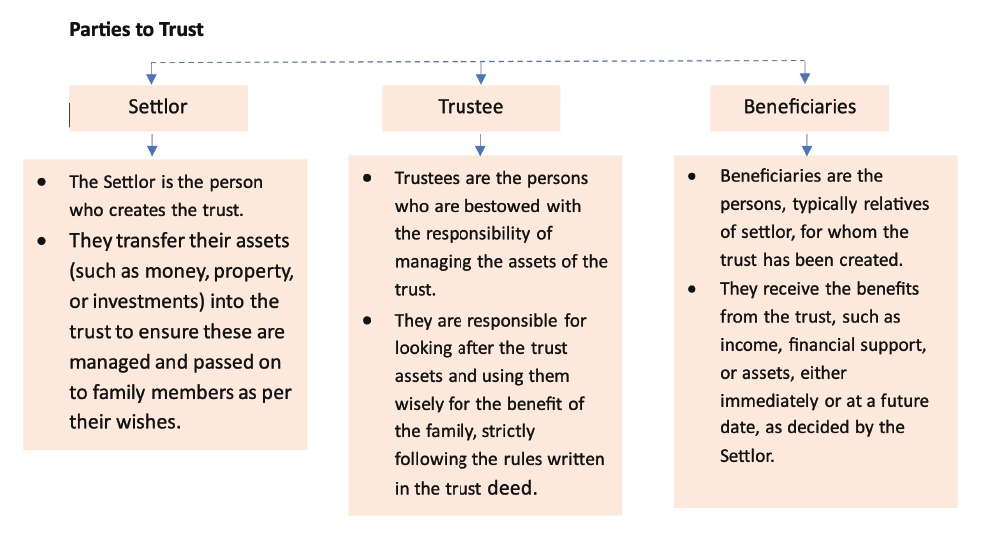

Parties to Trust

Why Private Family Trusts

Planning for the future is more than just dividing assets—it’s about ensuring that wealth serves its intended purpose, supports the family across generations, and reflects the values and vision of its creator. For affluent families, this requires a structured approach that goes beyond informal arrangements or traditional Wills. A Private Family Trust provides such a framework, offering clarity, continuity, and control over how wealth is preserved and passed on.

To better understand the relevance of a Private Family Trust, let us consider the case of Mr. A and his family –

Mr. A, aged about 60, is a successful entrepreneur who has built significant wealth through his operating business, real estate, and financial investments. His family consists of Mrs. A, his wife, who is a homemaker; their son, aged 30, who is actively involved in the family business alongside Mr. A; and their daughter, aged 32, who is married and settled separately.

With the objective of ensuring structured and long-term succession planning, Mr. A sets up a Private Family Trust, wherein –

Mr. A is a settlor, who has created the trust for the benefits of his family members and transferred his property to the trust.

Mrs. A, the wife of Mr. A and their son and a daughter are the beneficiaries of trust, who are going to receive the benefits from the trust.

Mr. P, a trusted friend of Mr. A is one trustee and Mr. A himself is another trustee, who are bestowed with the responsibility of managing the assets of the trust. Mr. A has nominated Mrs. A as a successor trustee, after his demise.

1. Preservation of Control Without Concentration of Ownership

In many families, wealth is created by a single individual but intended to benefit multiple generations. A Trust allows the settlor to retain strategic control over how assets are managed and distributed, without fragmenting ownership among heirs.

Mr. A transfers his portfolio of residential properties, mutual fund investments, and fixed deposits into a Family Trust for the benefit of his wife and two children. While the family receives regular income from rents, dividends, and interest, the Trustee decides when and how larger sums are invested or used. This way, Mr. A ensures that his wealth is preserved, grows steadily, and benefits the family over time—without giving direct ownership that could lead to mismanagement of funds.

2. Protection Against Personal and Business Risks of Beneficiaries

Inherited wealth is often exposed to the personal circumstances of beneficiaries—marital disputes, creditor claims, failed ventures, or litigation. Assets held in a Trust are ring-fenced from such personal risks, provided the Trust is properly structured.

If Mr. A undertakes a business venture that fails, the losses and creditor claims arising from such business risks do not impact the family wealth held in the Trust, as the he does not directly own the Trust assets.

Similarly, in the event of marital disputes or divorce involving Mr. A’s son, assets settled in the Trust generally remain outside the scope of personal claims such as alimony, since the Trust owns the assets, and not the beneficiaries i.e. Mr. A’s son. The son continues to receive benefits from the Trust as per its terms, while the core family wealth remains protected.

3. Avoidance of Inter-Generational Disputes and Litigation

One of the most common risks in succession is ambiguity—different interpretations of intent leading to prolonged legal battles. A Trust replaces ambiguity with clearly documented rules.

Over time, Mrs. A, the son, and the daughter may have differing expectations on reinvestment of business profits versus personal distributions. By clearly defining distribution rules and decision-making authority in the Trust Deed, Mr. A removes ambiguity and enables the Trustee to act impartially, thereby reducing the risk of future disputes or litigation even after his death.

4. Structured and Disciplined Wealth Distribution

A Trust allows the settlor to control the timing, purpose, and quantum of distributions, ensuring wealth is used responsibly rather than consumed prematurely.

Mr. A is concerned that his son may not manage large sums responsibly. By routing assets through the Trust, Mr. A specifies conditions on how and when the son can access funds—such as permitting usage only for education, housing, or business needs. The Trustee ensures these rules are followed. Such conditional control is not possible through a Will, making the Trust a practical rule book for the family.

5. Continuity Across Generations Without Repeated Succession Events

Unlike a Will, which triggers succession only once, a Trust can operate seamlessly across multiple generations without the need for repeated estate planning or probate processes.

After Mr. A’s lifetime, the Trust continues to hold and manage assets for Mrs. A and the children, and later for grandchildren if specified. This avoids repeated legal formalities or court procedures, ensuring wealth flows smoothly and seamlessly across generations.

6. Governance Framework for Complex Family Structures

Private Family Trusts enable the creation of formal governance mechanisms, such as trustee boards, investment committees, or protector roles.

As the family grows and members may live in different locations, Mr. A appoints Mr. P as Trustee with defined powers and oversight mechanisms. This governance structure ensures impartial decision-making while balancing family involvement and professional management.

7. Alignment of Wealth With Family Values and Vision

Beyond assets, a Trust can embed family philosophy, values, and long-term intent—transforming wealth into a purposeful legacy. Trust deeds may mandate philanthropic allocations, impact investments, or funding for family education initiatives.

Mr. A specifies in the Trust Deed that investments should prioritize stable, long-term growth and prohibits high-risk ventures such as cryptocurrencies or speculative trading. It also encourages funding for children’s education, charitable donations, and sustainable or socially responsible investments. This ensures that the family’s wealth is not only preserved but used in ways that reflect their principles and long-term vision.

If you were planning succession today, would you rely on a Will alone or consider a Private Family Trust? Let us know what you think — comments or write us on celebratinglife@ascentsolutions.in .

Conclusion

Succession planning is not about predicting mortality — it is about preparing continuity. The earlier it is structured, the greater the clarity, control, and confidence it provides to both the wealth creator and the next generation.

At Ascent Financial Solutions, we work closely with families to design succession structures that are not just legally sound, but aligned with long-term family vision and regulatory frameworks. In our next month’s newsletter, let us discuss more about the structure of the trust, roles of the parties and how Trust is different than will and gift.

Because wealth well-planned today becomes legacy well-preserved tomorrow.